Support CleanTechnica’s work through a Substack subscription or on Stripe.

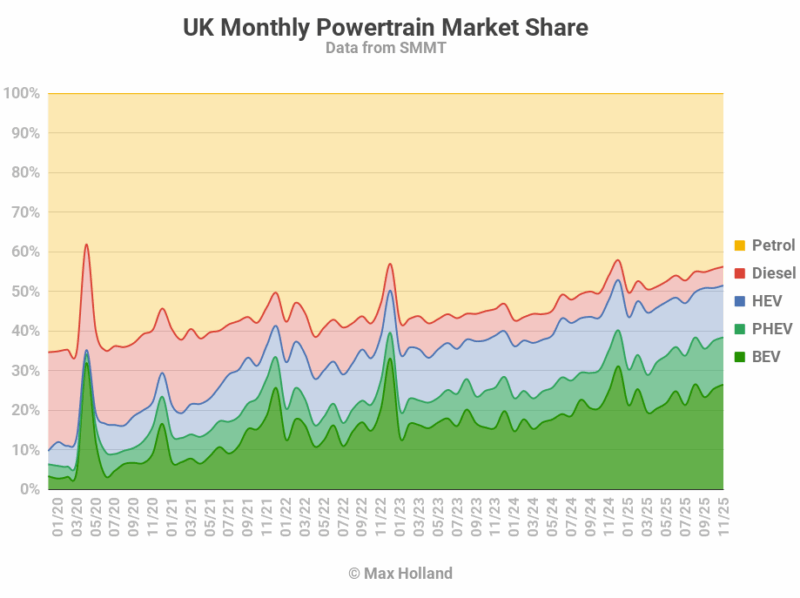

November saw plugin EVs take 38.4% share of the UK auto market, up from 35.3% year-on-year. BEVs grew in volume by just 3.6% YoY, while PHEVs grew 15%. Overall auto volume was 151,154 units, down some 2% YoY. Tesla was the UK’s leading BEV brand for the month.

November’s sales totals saw combined plugin EVs take 38.4% share of the UK auto market, with full electrics (BEVs) taking 26.4%, and plugin hybrids (PHEVs) taking 11.9%. These compare with YoY shares of 35.3% combined, 25.1% BEV, and 10.2% PHEV.

The combined effects of the reintroduction of modest purchase incentives for more affordable BEVs, plus the existing ZEV mandate, mean that the EV transition is in relatively good health in the UK compared to some European neighbours.

The YoY growth in share in November was somewhat modest, mainly because in the baseline month (November 2024) manufacturers were playing catch up with their BEV volumes, trying to meet the first year ZEV requirements, and avoid fines. This time around, most have presumably learned how to meet the requirement more steadily, and we won’t likely see such a big last minute rush.

Most manufacturers will also be balancing some need for a BEV sales push (to meet 2025 targets) whilst holding back any ‚Äúmore than required‚ÄĚ BEV sales until early next year. This will then help them get a headstart on the tighter mandate target for 2026 (‚Äú33%‚ÄĚ vs ‚Äú28%‚ÄĚ for 2025).

The proposed road-tax scheme of 3 pence per mile on BEVs is still in consultation, and anyway will not be implemented before April 2028 (even if it goes ahead). This is therefore unlikely to affect the pace of the UK’s EV transition in the near term.

In December, combustion-only powertrains’ combined share was 48.5%, the third consecutive month under half of the market (see graph below). Combined share may creep back above 50% in H1 2026, but should be permanently below 50% by H2 2026 and thereafter.

Best-Selling BEV Brands

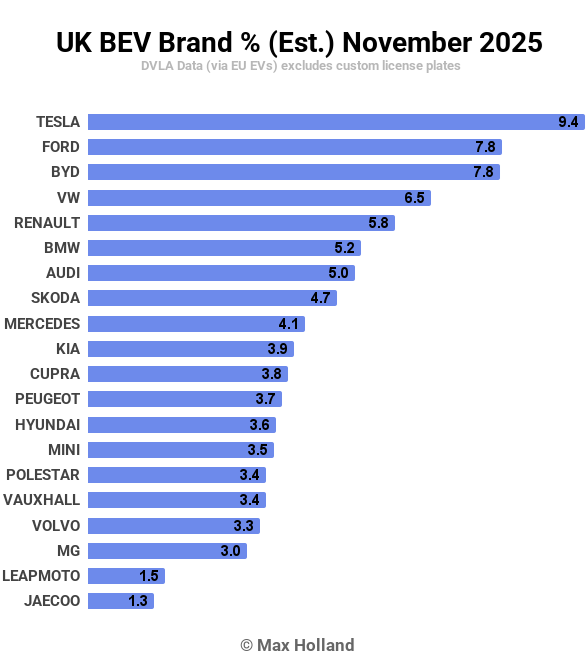

Tesla was back to volume in November (following a quiet October), and led the brand rankings with 9.4% of the UK BEV market.

Last month’s leader, Ford was pushed back to second in November, just ahead of BYD in third (both on 7.8% share).

Other than Tesla’s habitual feast-or-famine pattern, there were few significant changes in the top 20 rankings. At the bottom of the table, Jaecoo stepped back into the top 20, and its sibling brand, Omoda, stepped out.

It’s interesting to note that several of the best-selling models now start at or below (sometimes well below) the £30,000 price point. These include top 12 models like the Renault 5, Ford Puma, Skoda Elroq, BYD Dolphin and Dolphin Surf, and Vauxhall Frontera. All of these are capable of selling close to 1,000 units per month (or more).

Let’s now check the trailing-3-month rankings:

Having been close a month ago, Ford has now taken the lead from Tesla. With a strong December push, Tesla will likely soon take the lead once more. Ford has also been pushing hard since September to meet the ZEV requirement, so this is likely a temporary lead only.

Having been close a month ago, Ford has now taken the lead from Tesla. With a strong December push, Tesla will likely soon take the lead once more. Ford has also been pushing hard since September to meet the ZEV requirement, so this is likely a temporary lead only.

BYD is now in third place, ahead of the Volkswagen brand. Volkswagen has been erratic in the UK, often in second place for certain quarters, then going rather quiet in other quarters. This inconsistency is not reassuring.

Having assiduously delayed offering serious BEVs for almost a decade (not until the ID.3 in 2019, almost a decade after the Nissan Leaf), it might be Karmic justice to see BYD (long committed to plugins) overtake Volkswagen in the UK.

Outlook

The UK’s ZEV mandate and the new BEV incentive mean that the country is now making steady progress in the EV transition. Not as fast as many of us expected a decade ago, but at least moving decently in the right direction.

On the broader economic front, the UK is experiencing subdued conditions. Year-on-year GDP growth declined slightly to 1.3% in the third quarter, down from 1.4% in Q2. Inflation softened from 3.6% in October to 3.2% in November, while interest rates dipped from 4.0% to 3.75%. There was a modest recovery in manufacturing pre-orders, with PMI rising to 50.2 in November, from 49.7 in October

What are your thoughts on the UK’s EV transition? Do you see the Tesla Model Y maintaining its dominant position, or could more accessible models like the Renault 5, the BYDs, and Fords begin to overtake within the next couple of years? Please share your ideas in the comments below.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy