Support CleanTechnica’s work through a Substack subscription or on Stripe.

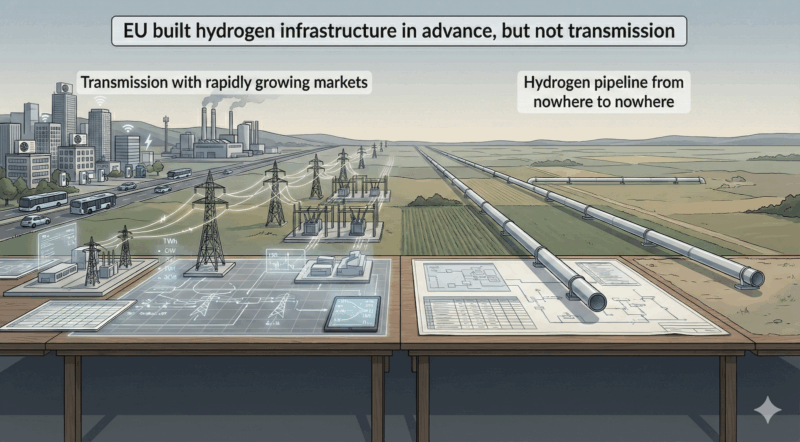

The most important policy lesson from the 400 km European hydrogen backbone segment with no suppliers and no offtakers—a pipeline from nowhere to nowhere—I wrote about recently is that decarbonization succeeds or fails on demand realism, not technological aspiration. Europe knew, as early as the late 2000s, that deep electrification of transport, buildings, and industry would sharply increase electricity demand. Conservative scenarios from transmission system operators and academic energy system models consistently showed electricity demand rising 40% to 70% by mid-century, with much of that increase front-loaded after 2020 as electric vehicles, heat pumps, and industrial electrification scaled. In Germany alone, credible projections showed annual electricity demand rising from roughly 500 TWh to between 650 and 750 TWh by the 2035 to 2040 timeframe. Those numbers implied a need for early, sustained expansion of transmission capacity to move renewable electricity from the north and east to industrial demand centers in the south and west.

That expansion did not happen at the required pace. Germany added wind and solar capacity far faster than it added transmission, with onshore wind capacity rising from about 27 GW in 2010 to over 60 GW by the early 2020s, while major north to south transmission corridors lagged by a decade or more. The result was predictable. Curtailment rose sharply. In some years, Germany curtailed more than 6 TWh of renewable electricity, with localized curtailment rates exceeding 10% in high wind regions. That is electricity that had already been paid for through feed-in tariffs or contracts for difference, electricity that could have displaced fossil generation or supplied electrification demand, but instead was thrown away because the grid could not carry it.

This failure to prioritize transmission had second-order effects that policy makers largely ignored at the time. Curtailment suppresses investor confidence in generation while inflating system costs for consumers. It also creates the illusion of surplus electricity, which hydrogen advocates then pointed to as justification for large-scale hydrogen electrolysis. In reality, curtailed electricity is a symptom of grid bottlenecks, not evidence of abundant cheap power. Building electrolyzers into constrained regions does not solve the constraint. It adds load that competes with electrification and pushes up local prices, while still requiring transmission investment to balance the system.

Both India and China have largely taken the opposite approach to Europe by building transmission ahead of demand, and the results are visible in lower long-term curtailment and faster integration of renewables. China has invested heavily in high-voltage and ultra-high-voltage transmission, with more than 40,000 km of UHV lines built to move wind and solar electricity from western and northern regions to eastern industrial and urban centers. While curtailment rates for wind and solar exceeded 10% in some provinces earlier in the 2010s, sustained grid expansion reduced national average curtailment to low single-digit percentages by the early 2020s, even as renewable capacity continued to grow rapidly. Recently curtailment has been edging back up, but China is building yet more transmission.

India followed a similar logic through coordinated national planning, accelerating transmission development alongside its renewable targets of 500 GW of non-fossil capacity by 2030. By prioritizing renewable evacuation corridors and interregional links, India reduced the risk of stranded wind and solar assets and limited curtailment that had previously affected tens of gigawatts of capacity. In both countries, periods of underused transmission were treated as a feature rather than a failure, enabling cleaner electricity to reach demand as electrification expanded and avoiding the persistent waste of renewable generation seen in systems where grid investment lagged behind supply growth.

A second lesson is that infrastructure-first thinking is a poor substitute for market formation. The hydrogen backbone was justified on the assumption that if pipelines existed, users would follow. That logic ignores decades of experience in energy systems. Demand follows price and reliability, not the existence of steel in the ground. Industrial users, including steelmakers, chemical producers, and refiners, require long-term price certainty and competitive parity. Green hydrogen delivered at $8 to $12 per kg cannot compete with fossil-derived hydrogen at $1 to $2 per kg (undelivered) or with direct electrification using $0.05 to $0.08 per kWh electricity. No amount of pipeline capacity changes that arithmetic. Building infrastructure without binding offtake agreements shifts risk from private investors to ratepayers and taxpayers, which is exactly what occurred as hydrogen pipeline costs were rolled into regulated electricity charges.

The same logic does not apply to electricity because broad and rising demand already exists and is largely insensitive to the specific location of individual infrastructure assets. Electricity demand is universal across households, commerce, industry, and transport, and it grows predictably as electrification advances. Electric vehicles, heat pumps, data centers, industrial motors, and electric furnaces do not require bespoke networks or new end-use technologies to justify grid investment. They connect to a system that already serves hundreds of millions of customers and trillions of kWh of annual demand. When transmission is built ahead of load, it enables lower-cost generation to reach existing customers, reduces congestion, lowers wholesale prices, and improves reliability. Even if utilization ramps gradually, the asset provides system value immediately by reducing curtailment, displacing higher-cost generation, and improving resilience. Unlike hydrogen pipelines, which require entirely new markets to materialize at specific nodes, electricity transmission serves an established and expanding market from the moment it is energized, making anticipatory investment a rational response to known demand growth rather than a speculative bet on future adoption.

A third lesson is that policy models must respect material and conversion losses throughout the energy system. Hydrogen pathways were repeatedly modeled using optimistic assumptions that compressed or ignored losses. Electrolysis efficiency was often assumed at 75% to 80% on a lower heating value basis, compression and storage losses were minimized, pipeline losses were dismissed, and reconversion losses in fuel cells or turbines were treated as secondary. When these losses are compounded, the result is stark. Delivering 1 kWh of useful energy through a hydrogen pathway often requires 2.5 to 3.5 kWh of electricity at the point of generation. Direct electrification typically requires 1.05 to 1.2 kWh. Policy that treats these pathways as interchangeable misallocates scarce clean electricity and drives up system costs.

The fourth lesson concerns opportunity cost. Capital deployed into hydrogen pipelines, storage caverns, and underused electrolyzers is capital not deployed into grid reinforcement, distribution upgrades, and firmed renewable generation. The European hydrogen backbone is expected to cost on the order of $80 to $100 billion if built out as planned. For comparison, $100 billion invested in transmission and distribution can unlock hundreds of gigawatts of renewable capacity and support tens of millions of electric vehicles and heat pumps. The returns, measured in avoided fuel costs and emissions reductions per dollar invested, are not close. Policy frameworks that fail to compare alternatives on a system basis will continue to favor capital-intensive but low-utilization assets.

A fifth lesson is that industrial decarbonization strategies must be anchored in global competitiveness, not regional aspiration. European green steel strategies assumed that customers would pay a durable premium of $100 to $200 per ton for hydrogen-based steel. That assumption conflicts with observed market behavior. Automotive and construction buyers operate in global markets with tight margins. Even a $100 per ton premium translates into tens of dollars per vehicle, which is material in a competitive market. Producers in regions with cheaper electricity, better transmission, and closer access to iron ore will undercut European producers if policy relies on premiums rather than cost reduction. Decarbonization policy that ignores trade exposure risks deindustrialization rather than transformation.

A sixth lesson is institutional learning speed matters. Evidence against broad hydrogen-for-energy use accumulated steadily over the past decade. Battery costs fell from over $1,000 per kWh in 2010 to under $150 per kWh by the early 2020s. Heat pump coefficients of performance improved while costs declined. Grid-scale storage scaled faster than projected. Hydrogen costs did not follow comparable trajectories. Yet policy frameworks were slow to adjust because models, funding programs, and bureaucratic mandates had been built around earlier assumptions. Effective climate policy requires mechanisms that force periodic reassessment against observed data, with the willingness to shut down or scale back programs that are not performing.

Finally, there is a lesson about sequencing. Electrification increases electricity demand. That demand should trigger early investment in generation and transmission, not follow it. Europe inverted that sequence. It built variable renewable generation rapidly without sufficient grid expansion, then attempted to absorb the resulting imbalance by creating hydrogen demand. A more effective sequence would have been straightforward. First, expand transmission and distribution to eliminate curtailment and reduce congestion. Second, electrify end uses that are already cost-effective, including light-duty transport, space heating, and low-temperature industrial heat. Third, allocate remaining clean electricity to niche hydrogen uses where no direct alternative exists, industrial feedstocks where hydrogen is the only molecule that will do. That sequence minimizes wasted energy, reduces total system cost, and limits hydrogen to roles where its inefficiencies are unavoidable rather than elective.

The hydrogen backbone episode is not an argument against ambition. It is an argument for discipline. Decarbonization is constrained by physics, capital, and time. Policies that assume demand into existence, ignore grid realities, or treat all clean molecules and electrons as interchangeable will repeat the same mistakes. The lesson is simple. Build the grid early. Let real demand pull infrastructure into place. Use hydrogen sparingly and as an industrial feedstock, not a Swiss Army knife. The transition will move faster and cost less if policy follows evidence rather than aspiration. Europe needs to drop its hydrogen dreams and commit to rapid build out of the mesh HVDC grid it needs.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy