Support CleanTechnica’s work through a Substack subscription or on Stripe.

Or support our Kickstarter campaign!

CATL is the largest battery producer in the world. Any move it makes is noteworthy. While CATL has been making sodium-ion batteries for some time, production commitment has increased dramatically in 2026. CATL introduced its Naxtra line of batteries earlier in 2025 and has now announced plans for volume production of sodium-ion batteries this year, with integration into production electric vehicles by July.

Battery technology is strategic for the world’s largest battery companies. Technology advancements enabled electric vehicles and energy storage to displace legacy solutions. Batteries now replace gas peaking power plants in utility peak demand and grid stability applications. This was demonstrated at the Hornsdale Power Reserve years ago, and in many parts of the world since then, including California, which now has 17 GW of battery storage installed, more capacity than any other jurisdiction outside of China. In China, battery energy storage systems (BESS) are major business, reaching 62 GW (141 GWh) by year end 2024. Battery energy storage is now a major market. In the first ten months of 2025, China battery exports were valued at $65 billion. Up until recently, EVs almost entirely used NMC batteries, while the energy storage market moved to lithium-iron-phosphate (LFP) batteries years back. That as changed with the introduction of LFP to more entry-level EVs. While EVs are still the largest segment of the battery market, energy storage has outpaced EV battery growth, increasing by 48% year over year. Electric vehicles and energy storage drove global lithium-ion demand in 2025 to 1,591 GWh.

Energy Storage Becomes A Battery Price Driver

In a recent 25 GWh battery storage auction, bids reached a low of $51/kWh for four-hour storage. Lithium ion has served growing markets well. Battery markets have reached high volume levels. LFP battery costs have reached their lowest costs so far. While some applications like energy storage have switched to LFP, until now sodium-ion batteries have not been produced at the same volume levels. The question is, why? By measures of Wh/kg, with the new Naxtra battery at 175 Wh/kg, sodium-ion chemistry has caught up with LFP.

Enter Lithium-Ion Price Volatility

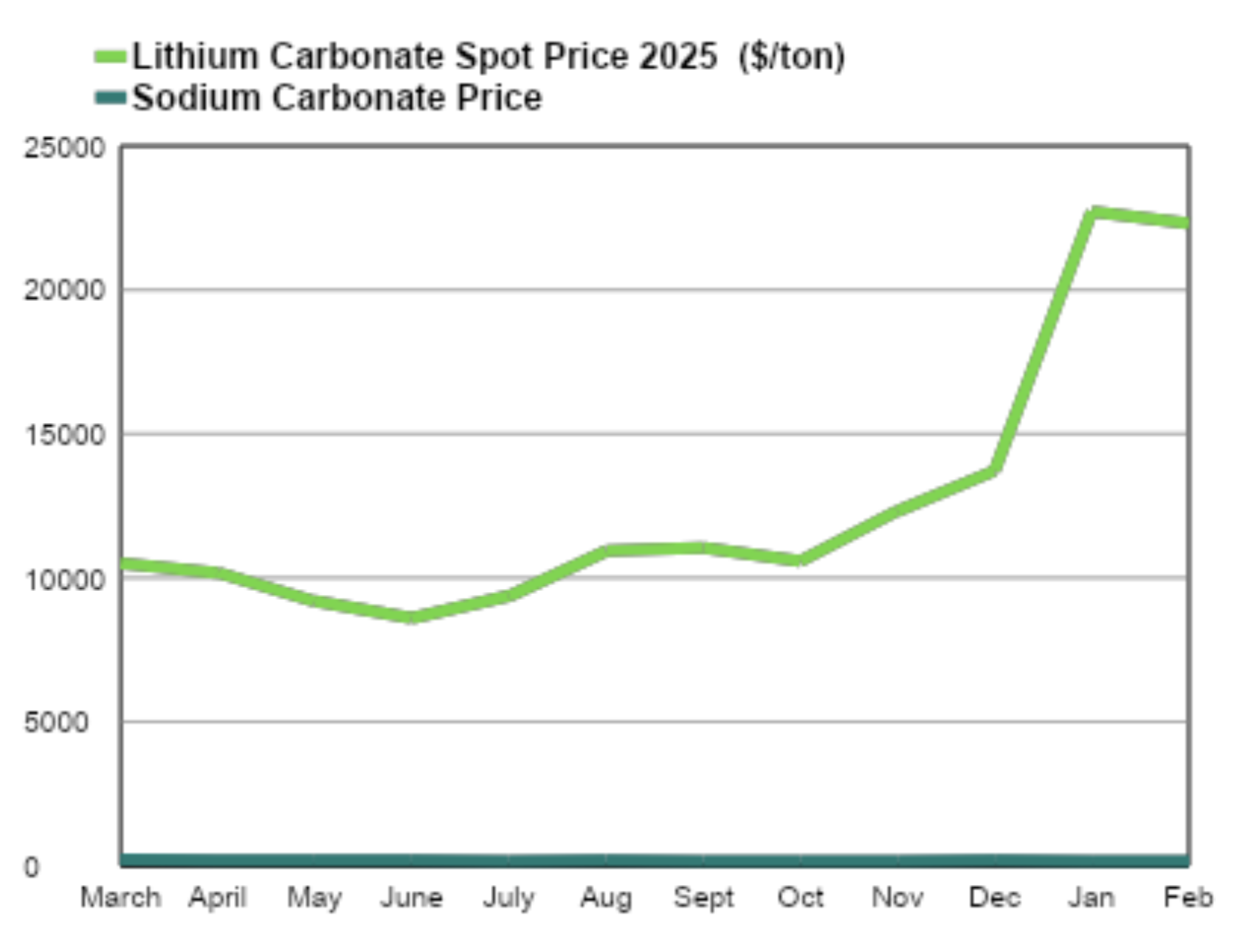

Lithium-ion price volatility and resource concentration may have caused a change in plans. In May of 2025, the spot price reached a low near $8,000/ton, and then rose 57% by November. Since then, by January 2025, lithium carbonate has risen to about $20,000/ton, or $22/kg. Lithium price volatility has returned.

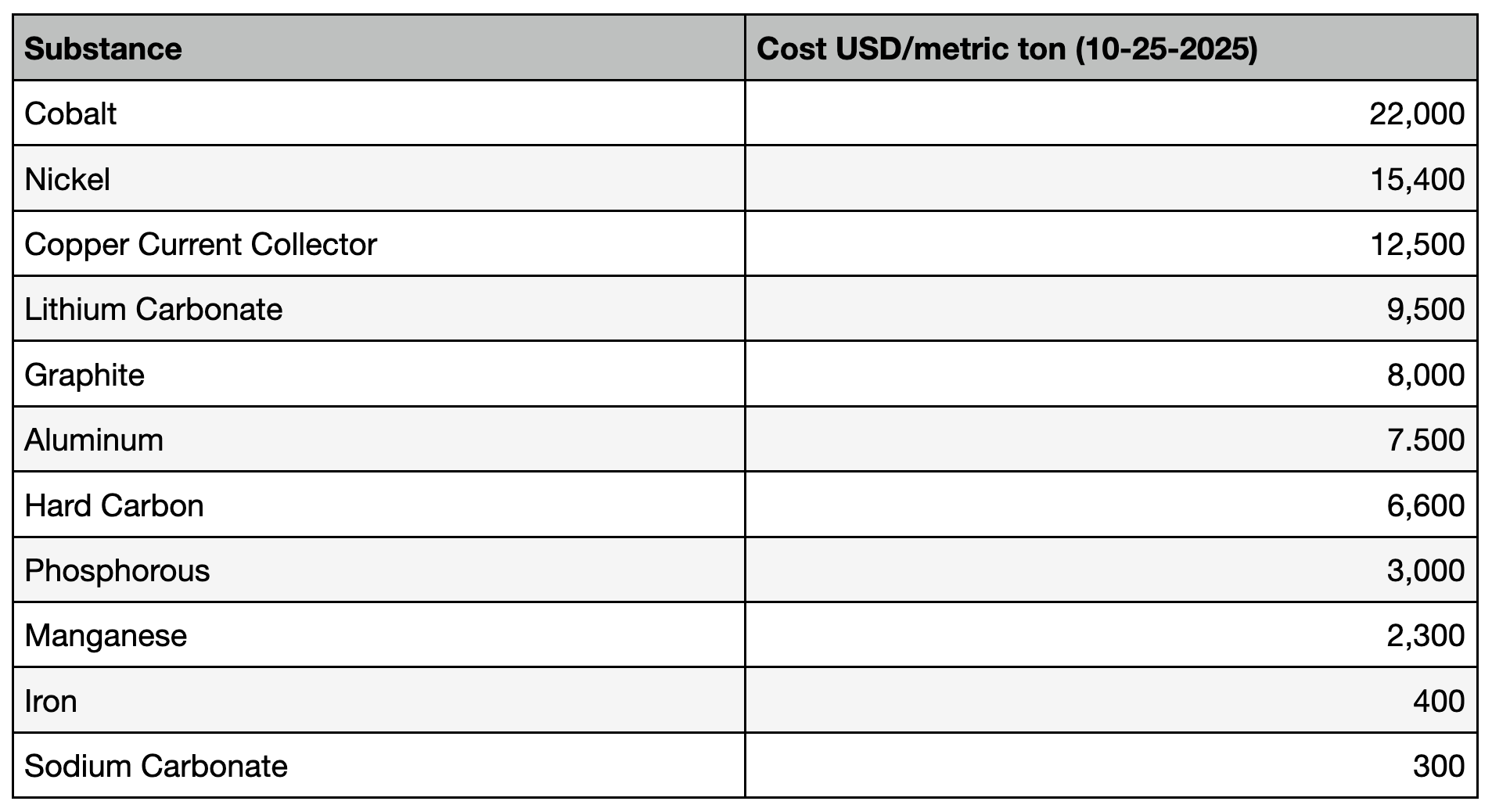

Battery production uses lithium carbonate, not lithium metal. The industry uses the term lithium carbonate equivalent (LCE) as a benchmark for lithium cost. Lithium carbonate is 5.32 times lithium metal in weight. A 1 kWh battery requires 160g of lithium, thus 850g of lithium carbonate (LCE). 0.85 kg of lithium carbonate at $22/kg is $18.70.

At that price, lithium is 37% of the cost of a $51/kWh battery. Lithium carbonate price volatility is a headache for volume production and represents a substantial percentage of battery costs when lithium costs rise.

LFP Cathode Providers Pinched

As battery demand reaches new heights, battery makers increase production of batteries like LFP that avoid nickel and cobalt. They have switched from NMC to LFP in high volumes to avoid the high materials costs, price volatility, and resource concentration of nickel and cobalt. Now, however, battery costs have fallen to the point where lithium price volatility significantly affects battery prices. To avoid this, major battery companies are switching to sodium-ion batteries, because sodium is more abundant, more widespread, and comes at a lower cost.

Lithium is a substantial contributor to cathode material cost. Lithium cathode providers are hardest hit, because their product cost depends heavily on lithium pricing. Rising lithium prices have created difficulties for LFP cathode material providers in China, causing them to raise prices and reduce capacity. CATL responded to cathode price increases by making a huge deal for LFP cathode material with Ronbay at a low price rather than with existing suppliers that raised prices. The amount of LFP cathode capacity slated for Ronbay is larger than Ronbay’s existing LFP cathode capacity by a factor of six. In an earlier deal with Ronbay, CATL pledged 60% of its sodium-ion cathode material capacity to Ronbay. So, CATL went with a provider that delivers both sodium and lithium cathode material.

Sodium Versus Lithium Material Availability & Cost

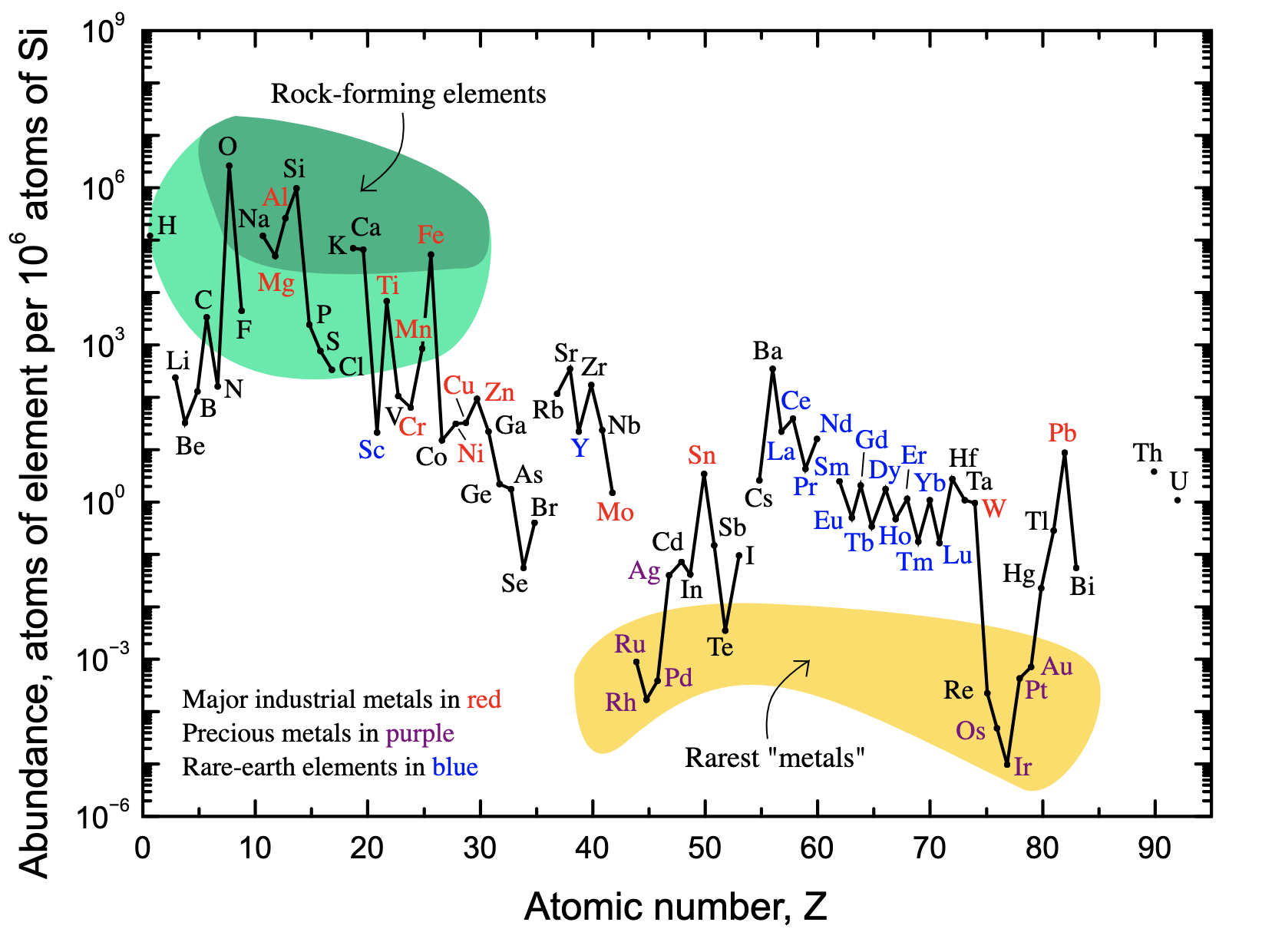

Sodium is the sixth most abundant element on Earth. Sodium-ion cathodes combine sodium and other abundant elements. The electrolyte contains sodium carbonate and a solvent. One type of sodium cathode, Prussian blue, contains sodium, iron, and nitrogen. In general, other sodium-ion cathodes consist of abundant materials like manganese. CATL uses a Prussian blue analog for the cathode. Layered oxides are another sodium cathode used for highest energy density. Sodium is two orders of magnitude more abundant and proportionally less expensive than lithium. First- and second-generation sodium-ion batteries use hard carbon anodes rather than expensive graphite. Cathode current collectors are less expensive aluminum, rather than copper. Overall, sodium material costs are in the single digits in terms of $/kWh. According to a recent paper by Yao, et al, a hypothetical lithium price shock in 2027 could advance sodium-ion costs to parity with LFP by 2030. That lithium price surge appears to be happening in 2026.

Another factor tipping the scales in favor of sodium is the emergence of self-forming anode technology. While lithium batteries use graphite, an expensive crystal form of carbon, early generation sodium-ion batteries used less expensive and widely available hard carbon. CATL Naxtra went further, using a self-forming anode and eliminating a carbon anode altogether. Self-forming anodes deposit sodium ions on the aluminum electrode current collector without any anode. Some calculations show hard carbon sodium-ion batteries have 30% larger volume than LFP. CATL claims Naxtra’s sodium self-forming anode is 60% smaller than an LFP anode. A standard lithium-ion battery has an anode thickness of 80 microns, cathode 60 microns, separator 14 microns, aluminum conductors 15 microns, and copper 8 microns. A 60% reduction in anode volume for a sodium-ion battery might result in about a 28% volumetric energy density improvement, eliminating the volumetric energy density difference with LFP. Hard carbon expense is eliminated. By comparison, LFP requires expensive graphite.

The Yao et al study shows long-term sodium-ion material costs well below $10/kWh for volume production, and production costs and volume not expected to equal LFP until 2035. However, CATL, BYD, and others are shifting to high-volume sodium-ion battery production now. This indicates that they believe sodium-ion batteries are ready for high-volume production competing with LFP from their own factories. The study assumes sodium-ion batteries could compete with LFP batteries by 2030 if there is a lithium price surge and sufficient sodium ion volume. The study expected that volume would not increase sufficiently before then. CATL has declared volume intentions this year to a wide range of applications, including vehicles and energy storage. It could be they both are right. CATL just changed the game by introducing volume earlier, because they want to maintain factory utilization while lithium prices rise. The strategy is to produce both sodium-ion and lithium-ion batteries, sustaining high factory utilization regardless of material price shifts. It is clear that CATL and BYD are betting on sodium-ion batteries for lowest cost and as a hedge against lithium volatility.

Conclusion

China has now reached a tipping point of over 50% electric vehicle sales. The battery market is maturing. Lithium made sense early on, with prices dropping, and when the market was growing and there were few alternatives. Lithium batteries progressed from NCA, to NMC, to LFP, lowering costs and increasing volume. Now that lithium batteries have become lower cost, lithium price volatility plays a large role in battery cost.

The largest battery companies in the world, BYD and CATL, now have significant investments in factory production. In order to maintain steady factory utilization, battery companies are shifting to the most abundant low-cost materials, with sodium-ion batteries to increase volume and further lower battery costs.

CATL intends to use self-forming anode technology and increase production volume to catapult sodium-ion to 50% of the LFP market. The company will supply a variety of battery technologies based on sodium and lithium in a “dual-star” market in which “sodium and lithium batteries shine brightly together.” Sodium-ion together with a variety of other battery types will fulfill roles across a spectrum of needs. As battery technology improves, sodium-ion technology will forge lower costs, erasing barriers to full electrification.

Editor’s note: Apologies, but a graph and a table were accidentally left out of this article initially. This was the fault of my own, not the author’s. — Zachary Shahan

Support CleanTechnica via Kickstarter

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy