Support CleanTechnica’s work through a Substack subscription or on Stripe.

After the usual December EV record sales peak in China, which coincided with an end-of-incentive sales rush (NEVs are no longer exempt from purchase tax this year), and adding to the Chinese New Year happening in February, EVs had an expected sales slump, down by 32% — which sounds like a lot, but considering that the overall market was also down 25% YoY, to around one million units, it doesn’t sound all that bad.

BEVs were down by 35% YoY in February, to 278,000 units, while the PHEV drop was also harsh (-31%). In the middle of all this pessimist outlook, EREV was the powertrain less affected by the slowdown (plugless models were down 19% YoY), having dropped only 16% YoY. This is thanks to the popularity of this kind of powertrain in large SUVs, which was the category less affected by the end of incentives.

These events pulled the year-to-date (YTD) tally to around 1.1 million units, and with March set to be the first strong month of the year, we should see Q1 end between 1.5 to 2 million units.

Share-wise, February saw plugin vehicles hit 45% market share. This is a full 5 percentage point result below where we were 12 months ago. Full electrics (BEVs) alone accounted for 27% of the country’s auto sales, also a significant drop from the 31% score of February 2025.

Still, this result pulled the 2026 share to 41% (in the same period last year, it was at 45% share). BEVs alone were also up, to 24% (27% BEV in Jan–Feb ’24), and considering that the last month of the quarter is usually a strong month, we can assume that the country’s plugin vehicle market share will end close to the 45% mark in Q1, and June should see it reach 50%.

(Could China finish the year close to 66%?)

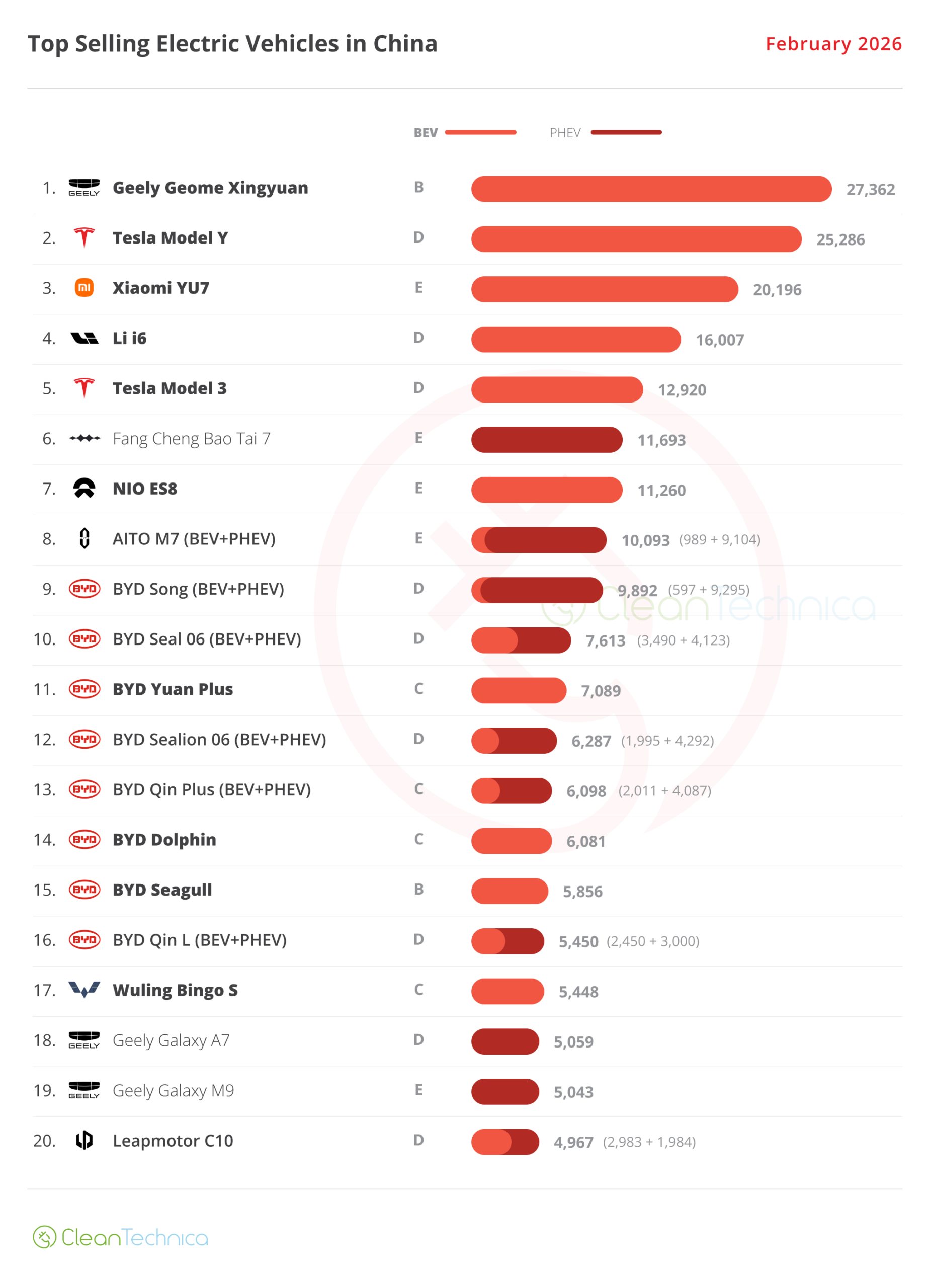

In the overall ranking, as usual, the beginning of the year had ICE models populating the top positions, but less than in January. Also rather surprising, the podium was all BEV, something unexpected this early in the year. The Geely Xingyuan was the best seller, beating everyone’s darling, the Xiaomi YU7, which ended the month in 3rd, and a surprisingly strong Tesla Model Y, which ended February in the runner-up position, no doubt thanks to the new, extended-wheelbase Model Y L.

See, Tesla? When you offer new stuff to consumers, your sales increase! I know, it seems more complicated than rocket science (or AI), but it would be worth having a look at it….

Behind these frontrunners, it is an ocean of ICE, with one EV island in the middle — which is in itself a surprise — the Li Auto i6. And Li Auto’s shark-like MPV-SUV combo deserves a few lines of reflection.

Li Auto success as a company has had its ups and downs, starting with tremendous success in 2020 thanks to the popularity of its innovative formula — big, comfy SUVs with a long-range EREV powertrain. This allowed it to be one of the most successful Chinese startups from the get-go, but around 2024, with the market shifting towards BEVs, Li Auto had to follow the market, so the company launched its first BEV, the bullet-train inspired mega-MPV … Li Auto Mega.

Despite the amazing specs and distinctive design, sales haven’t replicated the previous success, which led the startup to postpone the launch of the i8 full size SUV and its smaller sibling, the i6. And sales continued to suffer.

When they did launch those two models, in the second half of 2025, their success was quite different. While the bigger i8 failed to go toe to toe with the luxury full size category big boys (AITO’s M7 & M8, NIO ES8, Zeekr 9X, etc), the midsize i6 saw itself in a much less crowded space.

True, there are plenty of midsize SUVs on sale, but few exude the same level of luxury as the i6. The only other successful SUV that could compare to it is the Xiaomi YU7, but that one is sportier than Li Auto’s comfort-focused midsizer, and is generally priced higher than Li’s i6.

So it seems that Li Auto’s new star player has found its place in the market, and it will allow the startup to ride a second wave of success.

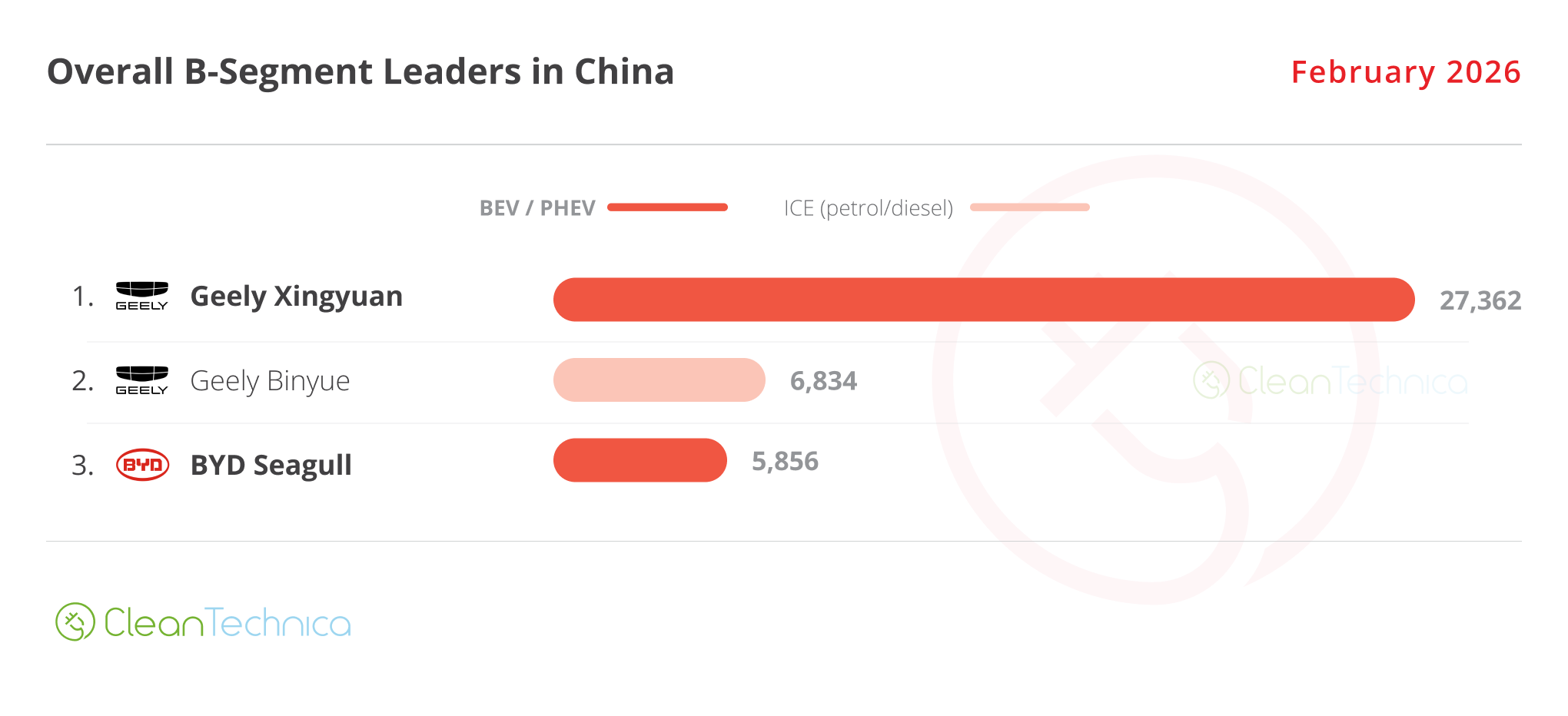

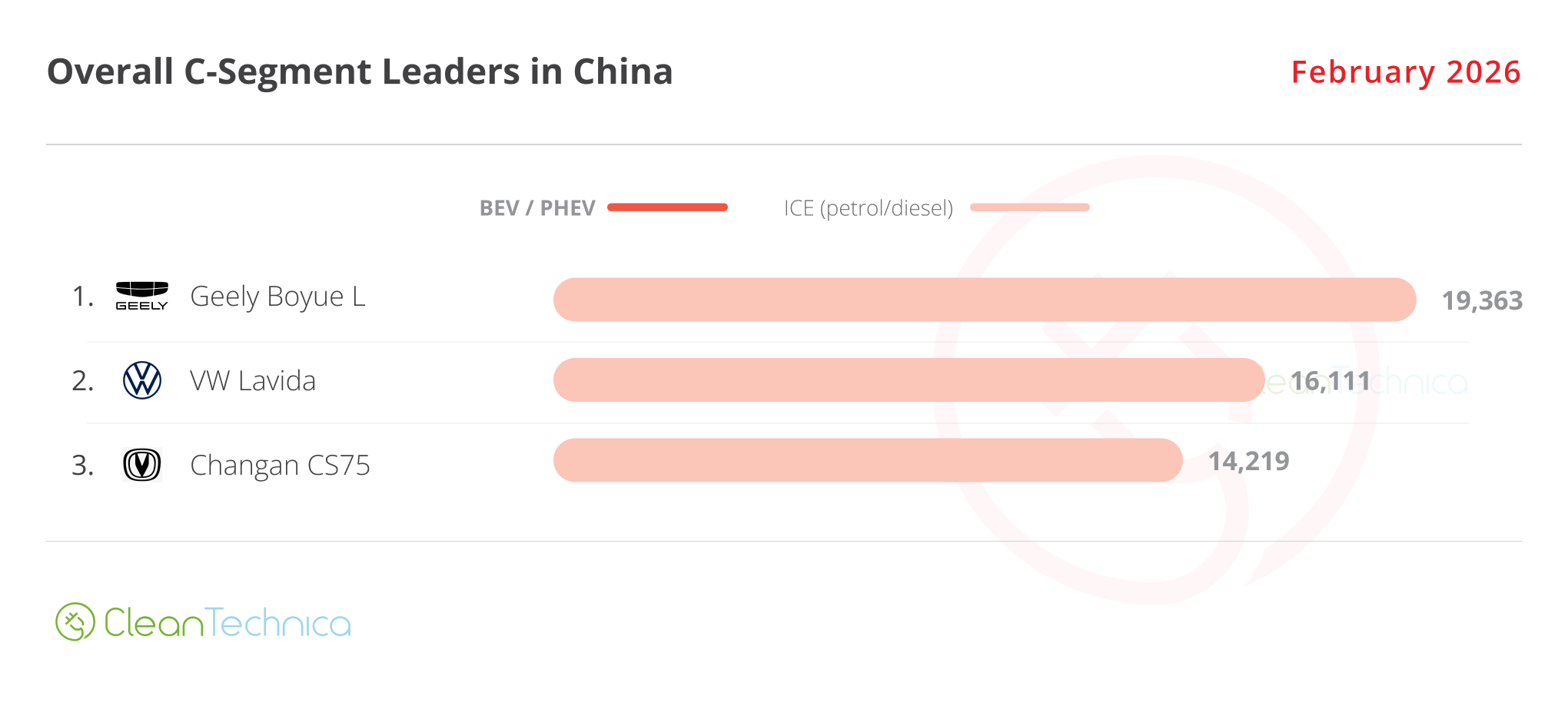

Looking at the best sellers in several size categories, things are returning to normal, as all but the C segment (compact cars) have plugins leading the way. In fact, the C segment was the only category where ICE managed to be the majority. This is a recurring topic, as it seems that the C segment is the hardest of all to convert into EVs.

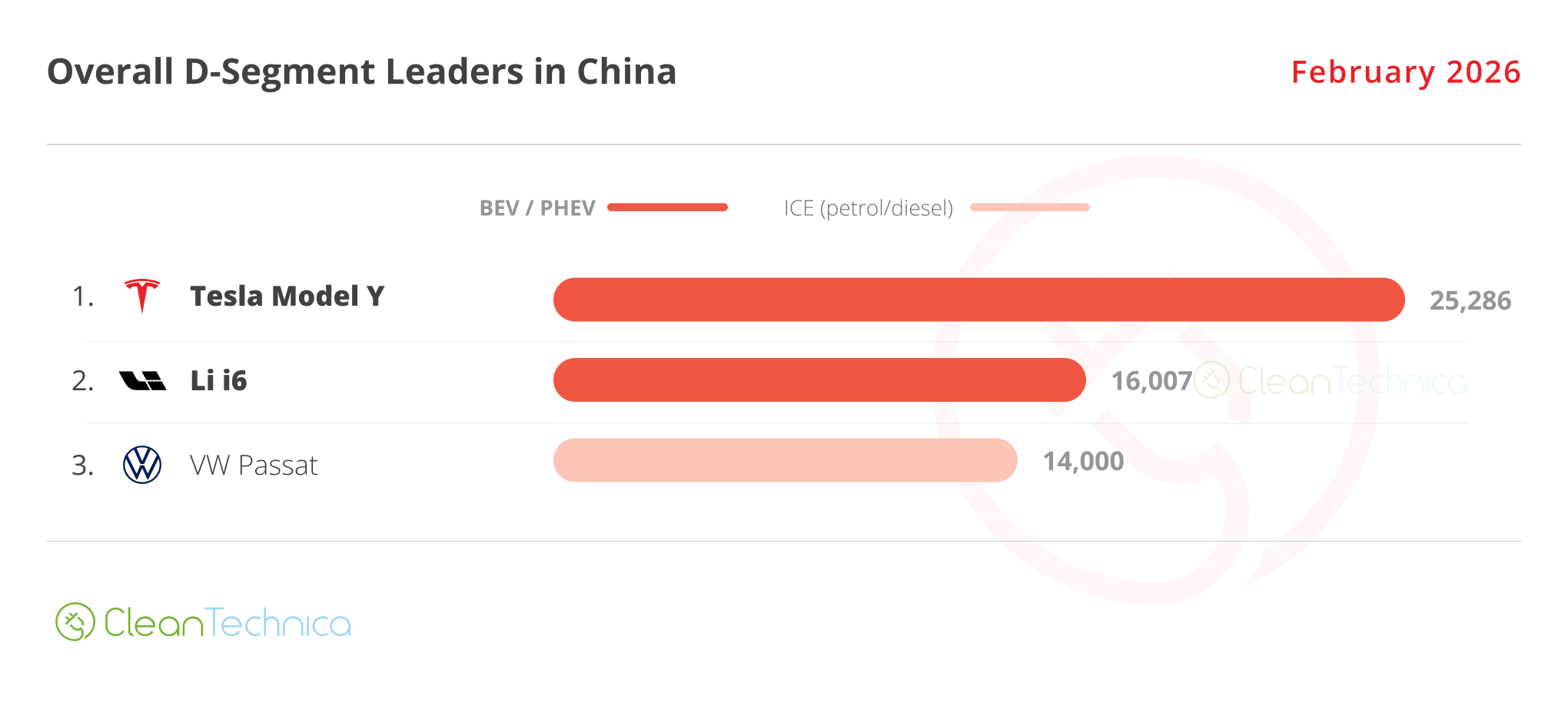

The biggest surprise was that the Tesla Model Y and Li Auto i6 stormed into the top two positions of the midsize category, while in the B segment (subcompacts), the BYD Seagull has returned to the podium. Will it be able to regain the upper hand over the Geely competitors?

After a surprisingly balanced January, Tesla managed to place two models in the top 5, an increasingly rare event. Here’s more info and commentary on February’s top selling electric models:

#1 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull money ($10,000 USD). At least, that’s how Geely’s internal memo might have described the Geome Xingyuan when developing its latest hatchback. And it’s got an interesting name, as Xingyuan translates as “wishing upon a star.” It seems that Geely had its wish granted. The small hatchback has finally given the Hangzhou OEM the much coveted Best Seller trophy, not only beating its BYD nemesis, but also everyone else. In February, the Geely model hit 27,362 registrations.

#2 — Tesla Model Y

The extended wheelbase version, imaginatively called “L,” seems to be helping the Model Y’s fortunes in China. In February, deliveries were up 216% YoY, to 25,286 units. True, comparing this month’s performance with February 2025 is distorted by the fact that a year ago, the Model Y was being affected by the launch of the refreshed version. But, comparing with what was going on two years ago, deliveries are more or less even. Though, considering Tesla’s current sales performances, that can already be considered a win….

#3 — Xiaomi YU7

Veni, Vidi, Vici. “I came, I saw, I conquered.” This could have been the YU7’s motto. Xiaomi’s crossover wasn’t able to keep its leadership spot from January in February, but nevertheless, thanks to 20,196 registrations, it again won the full size category leadership position. Besides already having that category trophy in the bag, expect the crossover to be a serious candidate for the overall leadership position in 2025, and with volume exports only planned to go into motion in 2027, expect a great year for the Chinese Ferrari.

#4 — Li Auto i6

After a strong January, things continue to go well for the midsize model, with the startup EV securing its first top 5 presence thanks to 16,007 registrations. With a high level of space, comfort, and luxury, for just $35,000 USD (for reference, the cheapest Tesla Model Y in China starts at $36,000 USD), the i6 offers an extensive list of equipment (air suspension, refrigerator, advanced self-driving — including Lidar), with a focus on space (three-meter wheelbase) and comfort, leading to a model that proposes full size luxury in a midsize-priced EV.

#5 — Tesla Model 3

Along with the Model Y, the Tesla Model 3 has been the lifeline for the Texan for a long time. But while the crossover sibling has been receiving regular updates, the sedan has been left out to dry. And while the 12,920 deliveries of February allowed it a top 5 presence, that number represents a 31% drop compared to February 2025. So, yeah, the midsize sedan is not holding on as well as its SUV sibling. With the price already low ($34,500 USD), maybe it would be a good time for Tesla to launch an extended wheelbase Tesla Model 3? I mean, today in 2026, the sedan still offers the same interior space as it did at its launch way back in 2017…. In a market where space is high on people’s priorities, that seems like a no-brainer.

Looking at the rest of the best seller table, the highlight comes from the BYD Yuan Plus, which benefitted from a recent refresh to jump into 11th, joining the rest of the BYD Armada. The brand placed 8(!) models, from 9th to 16th, in the top 20. The last one of them was the BYD Seagull, which is recovering from the incentive cut.

Other models on the rise are the #17 Wuling Bingo S, SAIC’s answer to the Geely Xingyuan and BYD Dolphin, while the sleek Geely Galaxy A7, the make’s answer to BYD’s midsize sedan offerings, joined the table at #18 thanks to 5,059 units.

Outside the top 20, because we are in the low season in China, there wasn’t that much to talk about, but we should highlight the following fact that proves the disruption that the incentive cut has brought to the Chinese EV market — the $5,000 USD Wuling Mini EV sold as many units (4,866 vs. 4,878) as the $65,000 USD Zeekr 9X….

The 20 Best Selling Electric Vehicles in China — January–February 2026

Looking at the 2026 ranking, the leader Xiaomi YU7 remained in #1, but below it, the Geely Xingyuan has shortened the distances significantly, so I wouldn’t be surprised if the small hatchback dethroned the crossover in March.

Below these two, the Climber of the Month was the Tesla Model Y, which jumped four positions into the 3rd position. Now the question is — will the Texan crossover be able to reach close to the top two next month?

Please place your bets now.

The other climbers in the top half of the table were the Li Auto i6, which climbed to 5th, and the veteran BYD Song, which was up one spot to 8th. Still in the BYD stable, the Seal 06 sedan jumped three positions into 10th, while the Tesla Model 3 did even better, coming out of nowhere into 9th, or one place above of its final standing in 2025. Will the Tesla sedan be able to stay there?

In the second half of the table, there were also major movements, with the highlights being the BYD Sealion 06 going up three spots, into #13, while two models rejoined the table — the #15 BYD Dolphin and #20 BYD Qin L. Additionally, the new Wuling Bingo S made its debut on the table in 17th place. Will Wuling’s new baby be a regular in the top 20?

Looking at the overall manufacturer ranking, after BYD’s shock crash in January, there was a lot of expectation to know what would happen in February.

Well … while the trend across the top 10 was slowing sales, BYD didn’t slow down, it crashed. Again. Sales were down 64% YoY. But … the explanation could be linked to March 6th and the unveil of BYD’s new technology suite, designed around the 2nd generation of the Blade battery. With amazing specs, and the added bonus that this new technology would be more spread out than previously thought, this could be just the Osborne Effect taking its toll.

To be continued…

Looking at the few gainers in the top 10, Tesla (+43% YoY) was by far the highlight, but Chery (+10%) and BMW (+1%) also deserve a mention. In the case of the Bavarian, it will be interesting to see of the new iX3 will have any impact in China. So far, the only foreign legacy brand able to sell EVs in decent volumes in China has been Nissan. Will BMW be the second?

Outside this top 10, a mention goes out to NIO, which is continuing to grow fast (+65% YoY) thanks to the success of its new ES8. Can these volumes continue?

On the losers side, Xpeng is crashing (-59% YoY, to 11,608 units), a surprising result for a startup that was among the hottest brands last year.

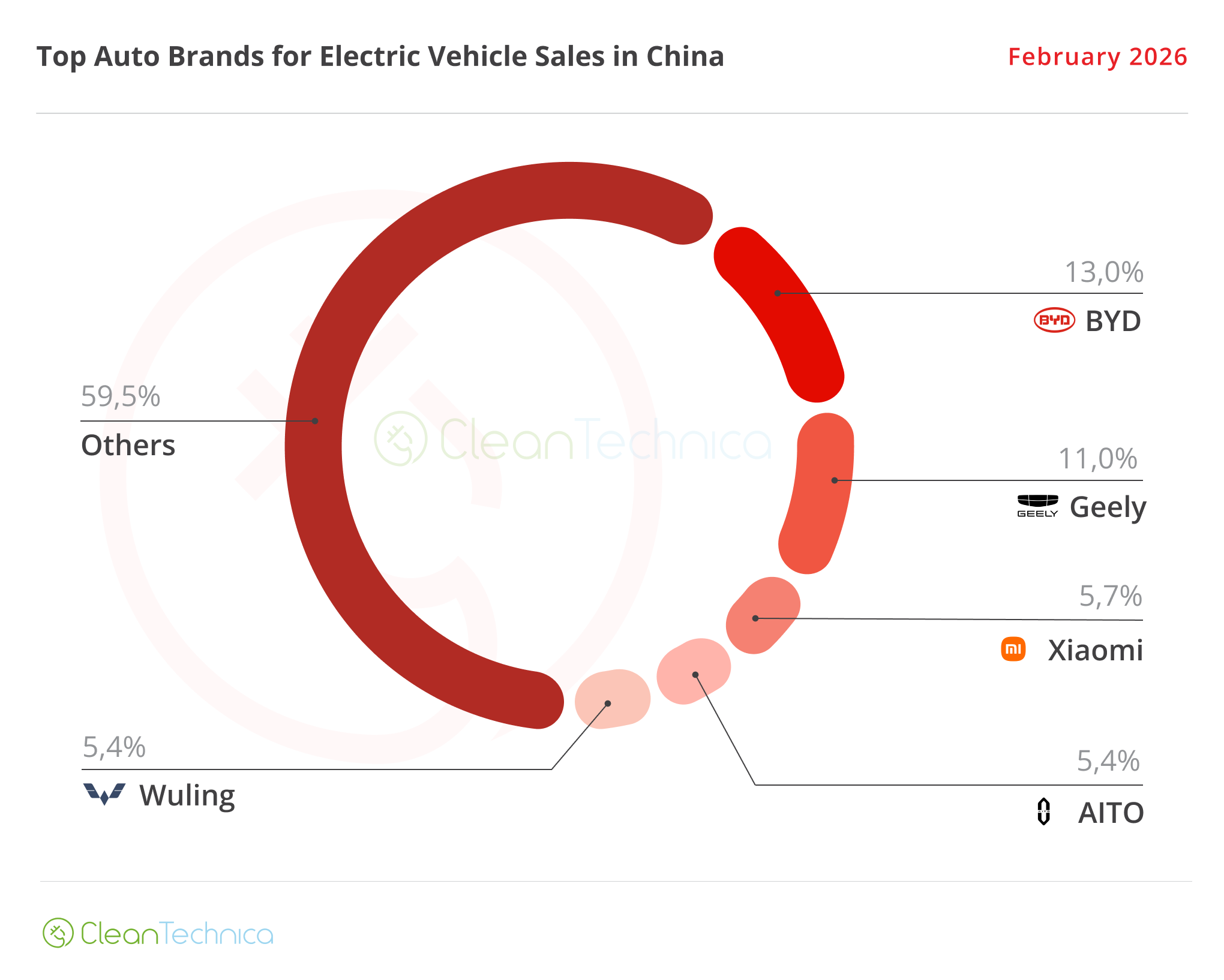

Auto Brands Selling the Most Electric Vehicles in China

Looking at the auto brand ranking, there’s some news, but not at the top. Leader BYD (13%, up from 11.5%) and runner-up Geely (11%, up 0.6%) have gained share and will probably fight for the top position, during the remainder of the year.

Things get more interesting below, though. Despite losing share, Xiaomi (5.7%, down from 6.5% in January) climbed one position, to 3rd, since previous bronze medalist, AITO, lost even more share.

#5 Wuling (5.4%) hung on, and is now some 100 units behind #4 AITO. So, we might see SAIC’s most popular brand jump into 4th…

… unless #6 Tesla (5.4%), which is fewer than 1,000 units behind AITO, experiences a strong peak month in March and surpasses both brands. It could even be the case that Xiaomi’s 3rd spot ends up in danger….

Behind Tesla, another brand is on the rise. #7 Li Auto increased its share (5.2%, up 0.6%), so it too could have a shot at joining the top 5 in March.

Auto Groups Selling the Most Electric Vehicles in China

Looking at OEMs/automotive groups/alliances, BYD is leading, with 17.2% share of the market, up 1.4% compared to the previous month. Meanwhile, #2 Geely, despite gaining 0.4% share and getting up to 15.9%, has seen BYD put more distance between it in the race for #1.

Far from runner-up Geely, #3 SAIC (9.4%, down 0.4 percentage points) has lost share, as several of its brands (MG, IM Motors, Shangjie) had a slow February.

Lucky for them that the most direct competition didn’t fared much better, as Xiaomi (5.7%) and Seres (5.5%, down from 6.7%) dropped even more than the Shanghai-based OEM.

Changan (5.5%, up 0.3%) profited from all of this and joined the table in 5th, kicking Seres out of the top 5.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy