Support CleanTechnica’s work through a Substack subscription or on Stripe.

Makings EVs Great Again — EV Share jumps to 33% in Europe!

Thanks to a number of factors (new models, high gas prices, mass arrival of Chinese models, etc.), EVs have picked up again in Europe. Close to 385,000 plugin vehicles were registered in Europe in April, 262,000 of them being pure electrics (BEVs). Overall, plugin vehicles were up 35% YoY.

The overall market also had a positive month in April, rising 7% YoY to over 1.1 million units. That improved the YTD performance and brought it back into positive numbers, +5% YoY.

Looking at the April powertrain breakdown, one can see that ICE vehicles are melting (with petrol down 15% YoY, to 22% share, and diesel down 17% YoY, to 7% share) and plugless hybrids are now the most popular powertrain (36%), still managing to grow slightly above the market average (+13%). However, it’s really plugins that are the ones pulling the market upwards — with BEVs surging 42% to 23% share and PHEVs going up 23% to 10% share.

But the two plugin powertrains seem to be seeing contrasting trends. While it seems that PHEV growth is decreasing (April’s 23% growth rate is the lowest of the past 12 months), BEVs are picking up (they jumped 42% YoY, which the second best growth rate of the last two and a half years).

And that shift is also visible in the BEV vs. PHEV sales breakdown, with BEVs having 68% of all plugin sales in April. That pushed its yearly average to 67%.

Adding the 36% market share of HEVs to the 23% of BEVs and the 10% of PHEVs, this means that 69% of all new cars in Europe had some sort of electrification.

With BEVs pulling the market upwards, the year-to-date share for BEVs went up to 22% (32% for PHEVs and BEVs combined), which is already higher than the 2025 final result (20% BEV share, 29% adding PHEVs). This is an encouraging sign if we want to be close to 100% PEV share by the mid-2030s.

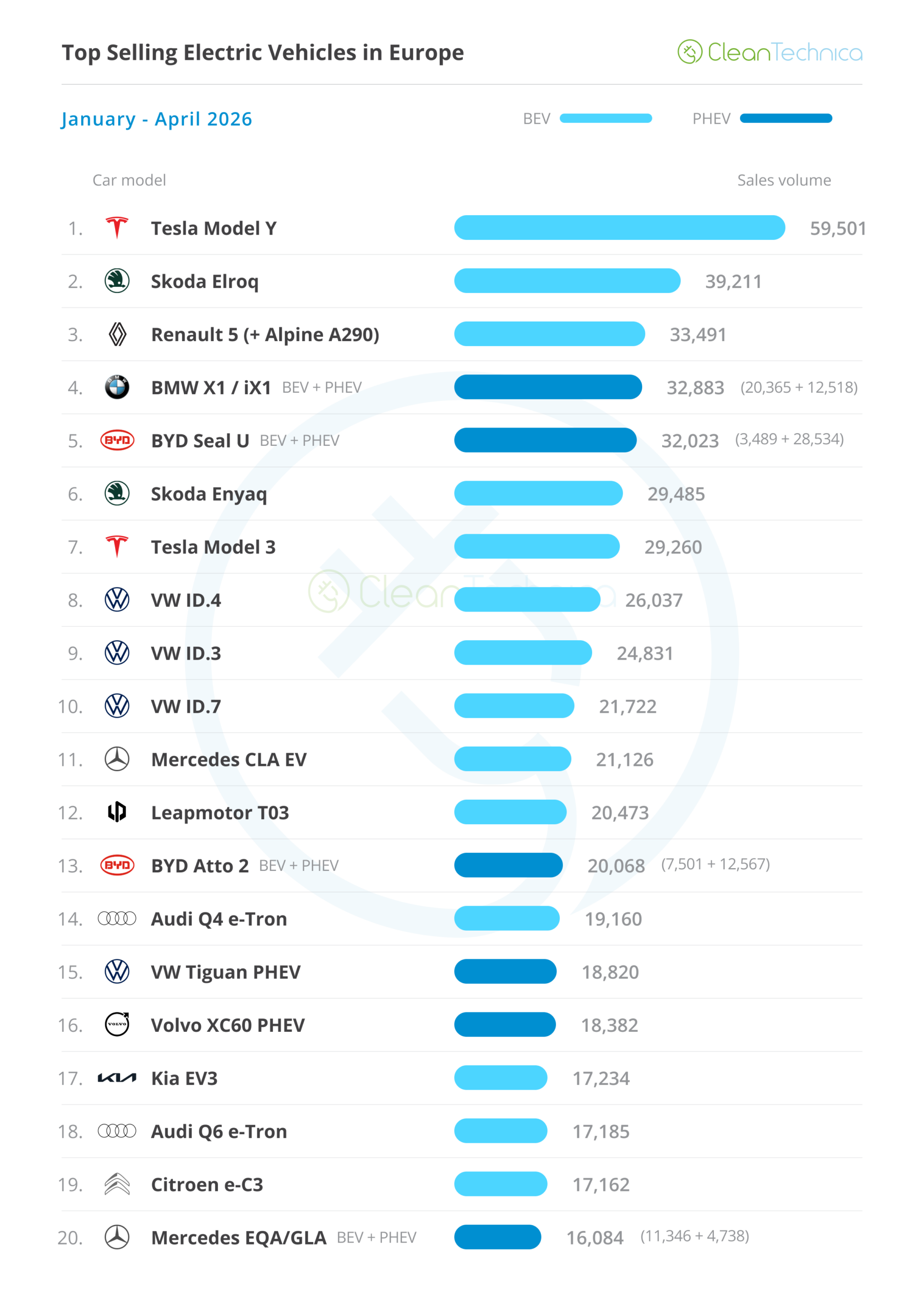

Looking at the best selling models, the big news this month was Skoda placing two models in the top 5. Here’s a more detailed analysis of the top 5 EVs this month:

#1 Skoda Elroq — In an off-peak month for Tesla, the Elroq won another monthly best selling model title in April, thanks to 10,817 registrations, which is a 34% increase YoY. Looking ahead, towards the second half of 2026, the problem for the Czech crossover is that in the second half of 2026, a new, smaller, and more affordable Skoda crossover will land. Called the Epiq, that model risks stealing lots of sales from the current star player of the Skoda lineup, as it will be simultaneously cheaper and more modern than the Elroq. So, while the first half of 2026 might see the Elroq run with the Teslas, later in the year, we could see it lose some speed.

#2 BMW iX1/X1 PHEV — The German twins are in cruise control, winning another podium position in April thanks to 9,447 registrations, a 13% increase YoY. Benefitting from favorable lease rates to help things along, the BMW crossovers are the brand’s bread and butter models, at least until the much hyped iX3 gets up to full speed. With a deep refresh coming later this year, promising to transform them into baby Neue Klasse vehicles, expect both, but the iX1 in particular, to upgrade their specs. That will make them more interesting than the current versions and allow the Bavarian brand to keep its compact models as podium material.

#3 Renault 5 (inc. Alpine A290) — Renault’s star player delivered 8,954 sales in April, with the iconic hatchback increasing its sales year-on-year by 29%. Looking at its 2026 performance, with production already ramped up and demand now at cruising speed, now is the time for the French twins to show their true value. Will they replicate the success of their Renault Zoe predecessor? No matter how attractive the 5 is, the truth is that in 2026, its space on the market will be squeezed not only by external competition (VW ID.Polo, Cupra Raval, etc.), but also by internal competition, with the equally cute new Twingo stealing sales from below and the 4 crossover doing the same from above. And let’s not forget the Nissan Micra, which is basically a Renault 5 in a Manga costume….

#4 Skoda Enyaq — Skoda’s original electric crossover managed to reach the top 5 thanks to a refresh and attractive deals. It had 8,160 registrations in April, a 52% sales increase year-on-year. There were thus two models from the Czech make in the top 5. This performance shows that despite the risk of the Elroq cannibalizing a portion of its sales, the Enyaq still had enough demand on its own to return to the top 5 — a positive omen for the future cohabitation of the Elroq and the Epiq?

#5 BYD Seal U (BEV+PHEV) — The Chinese SUV hit 8,101 registrations last month, meaning that while the BYD’s veteran star is already fading in China, at least until the new generation Ultra body is up to speed, the old generation is still able to reach the top 5 in Europe (a bit like when veteran football/soccer players #ahem# Cristiano Ronaldo #ahem# leave the top leagues and semi-retiring in less competitive leagues…). April’s 5th place finish was much thanks to generous discounts, but still, with the model’s development costs now well behind it, BYD can afford to go into hard discount territory with this one.

Outside the top 5, the highlights came from both Germany and China.

Starting with Germany, Mercedes’ star player, the CLA EV, clocked 6,686 registrations, a near-record result, no doubt thanks to the new station wagon body and cheaper versions. In 2026, the German make is pulling out all the stops to be in a better position in 2027 than it was in 2025. And for that, besides the CLA, the three-pointed-star brand is ramping up both the new GLB EV seven-seater and the GLC EV midsizer.

Sure, volumes are still relatively small (the GLB had 1,990 sales and the GLC had 1,211 sales), but the truth is that both are still in their second month…

… but that is no excuse for BMW, which already placed its brand new iX3 inside the top 20 (4,449 sales), despite also being in only its second month on the market. That is one of the things pushing back Mercedes compared to its Bavarian rival. Mercedes takes its time ramping-up production, while BMW does not.

As for China, besides another strong result from the Leapmotor T03 (12th, with 5,573 registrations), with the rumormill saying that the next-generation T03 will be the base for the next-generation Fiat Panda and Citroen C2 city cars*, the other highlight is the BYD Atto 2 (Yuan Up in Euro-spec). The Atto 2 was 9th in April, with 6,781 registrations, with 5,000 of them belonging to the new PHEV version. Will the new, PHEV-only Dolphin G, set to land soon in Europe, be able to duplicate this result? (*Will this be a trend, Stellantis? Will all your future EVs be based in Leapmotor models?)

If the Dolphin G can duplicate, expect the Renault Clio Hybrid, Peugeot 208, Dacia Sandero, and Toyota Yaris Hybrid, among other ICE subcompact models, to suffer some degree of cannibalization from the new model, which will be the only B-segment hatchback to have a PHEV powertrain.

Priced right, say around 23,000 euros, and one could say that it will be another nail in the ICE coffin. And BYD’s third model on the table.

This is one of the things that makes BYD so impressive. Its lineup depth is unbeatable, allowing the company to pick and choose different models according to each market’s personal tastes, and when the brand doesn’t have anything to suit a certain market’s tastes, it just uses the quality of its R&D to create something tailor-made, like the Atto 2 PHEV or the future Dolphin G.

Remember when you were that productive, Volkswagen?

Outside the top 20, the highlights also come from Asia.

Toyota is ramping up its C-HR+, a new BEV unrelated to the hybrid C-HR but with the same philosophy and market position. In only its second month on the market, the Japan-made EV was #21, with 4,130 registrations, so expect a top 20 position in May.

The other highlights came from Korea, with the small Hyundai Inster scoring 3,762 sales, a new record for the bug-eyed EV thanks to fresh discounts. As for Kia, it landed its new-generation Kia Soul EV2 with a promising 1,638 registrations, so the B-segment is sure to have another strong player here. And with the appealing Hyundai IONIQ 3 set to land soon, Hyundai–Kia sure looks to be prepared to put their cards on the table in this category.

Still in Korea, a mention goes out to MPVs and the recent Kia PV5, which scored a record 1,045 registrations, its first 4-digit result. Sure, it is still far below the category leader, the VW ID.BUZZ (2,500 units in April), but with prices starting at 33,000 euros, a significant step below the 50,000 euros of the German MPV, the potential is there for the PV5 to become the sales leader in MPV-land.

Looking at the 2026 ranking, the major change in the top positions was the four-position drop of the Tesla Model 3 into the 7th spot. But that was to be expected, as it was the first month of the quarter. In fact, one can say that Tesla had a positive month — even the Model 3 increased its sales YoY (2,771 units in April, a 16% increase over April 2025).

Has Tesla bottomed out? It sure seems like it. With BEV demand back in the fast lane, we could actually see the Model 3 return to the podium in 2026. Although, that will depend also on the behavior of the Renault 5 and the BMW X1 twins. Heck, we might even see the Skoda Elroq lose speed and witness a four-horse race for the silver and bronze medals….

Bring on the popcorn, because this looks to be fun!

As for the remaining changes, the Mercedes CLA EV was up again, to #11. The Audi Q6 e-tron climbed to #18, while the Mercedes EQA/GLA PHEV twins joined the table at #20. The German make now has two representatives in the top 20, something that hasn’t happened in a long time.

But the highlight was the BYD Atto 2 jumping into 13th, much thanks to the new PHEV version, which represents 63% of all of the model sales this year. So far, the Atto 2 PHEV has no direct competition, allowing it to steal sales from ICE models in the small crossover category.

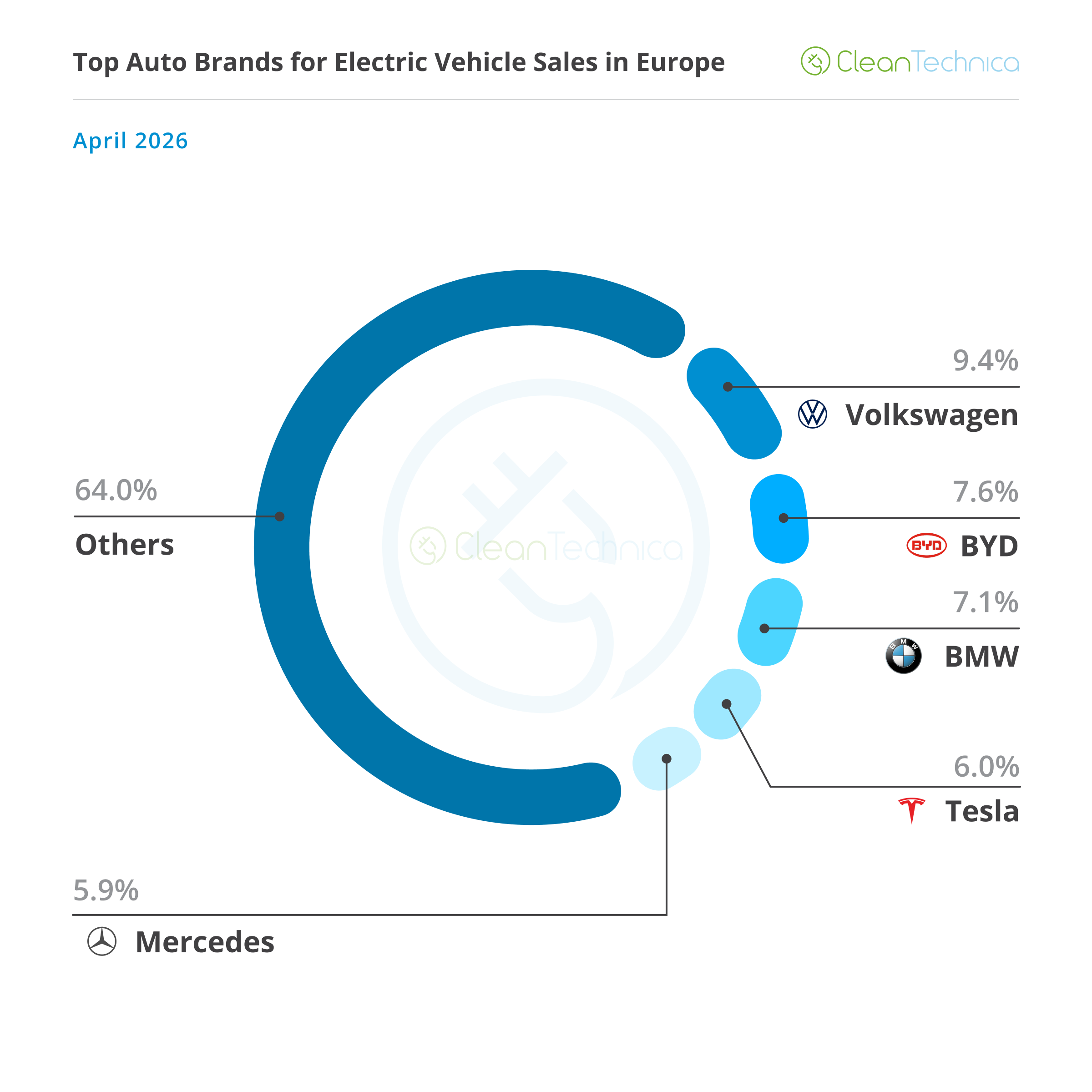

Having a quick look at April’s overall brand ranking, the highlight is Skoda (+10% YoY), now 2nd thanks to 76,000 registrations. It is only behind the all-mighty Volkswagen, all while a number of established brands are feeling the pinch (#11 Hyundai was down 12% YoY, #12 Ford dropped 13%, and #20 Nissan was down 10%).

Sure, it’s still not the horrific numbers seen in China, but the European market is still around halfway down the path that China is on right now, so 50% drops could become a reality in a not too distant future.

So, in a growing market, who is pushing the market upwards? China and Tesla (+47% YoY).

Chinese OEMs in April were up 125% YoY, to 9% share, contrasting with the 4% share they had in April 2025. Highlights were #17 BYD (up 115%, to 27,000 registrations, no surprises here) and … Chery (OEM), with the total of their brands (Jaecoo, Omoda, Chery…) surging 322% YoY!

But wait, there’s more! Startup Leapmotor, 29th on the table with 9,000 registrations, jumped 404% compared to April 2025!

(With this in mind, one won’t find it that strange that Stellantis is on its way to becoming a sort of Leapmotor coachbuilder, picking up from the original models and reskinning them according to each of the brand’s design DNA. Imagine that — a new Chrysler Pacifica based on the new Leapmotor D99 MPV, or an Alfa Romeo SUV based on the Leapmotor C10. The possibilities are endless!)

As for the plugin auto brand ranking, the leader, Volkswagen, remained in the lead (9.4%), holding a comfortable advance over a rising BYD (7.6%, up 0.3%). Will BYD be able to go after Volkswagen in Europe? One thing is certain — with local competitors (Renault, Stellantis, etc.) losing scale by the day, BYD looks to be the only brand able to pressure VW’s reign in Europe. Place your bets.

The biggest change happened below BYD. As expected, Tesla (6% share, down from 7.1% in March) lost the 3rd position to BMW (7.1%, up 0.1%) and is now in the 4th position. With the iX3 now starting its career, expect the German make to be a serious candidate in the race for the 3rd spot.

As a note, the 2025 podium was as follows: #1 Volkswagen; #2 BMW; #3 Mercedes. So Mercedes can already kiss goodbye to its podium presence, and as for BMW … let’s see how it goes.

Speaking of the three-pointed-star make (5.9%, up from 5.8% in March), in April it returned to the 5th position, surpassing Audi (5.8%).

The Stuttgart brand has a LOT of fresh metal coming in this year (GLB, GLC, VLE, VLS, C-Class…), but its 5th position is in danger because of rising Skoda (5.6%, up 0.1%). While the Czech brand is still 7th, it will introduce two brand new BEVs in 2026, the small Epiq and the large Peaq. Both will surely increase the total volume of sales from the brand significantly, so expect them to increase its market share, possibly bring it to a top 5 spot.

This would keep BMW as the only premium brand in the top 5, which would speak volumes about the democratization of the EV market and helps to shed that “cars for the elites” stereotype that some wanted to associate with EVs.

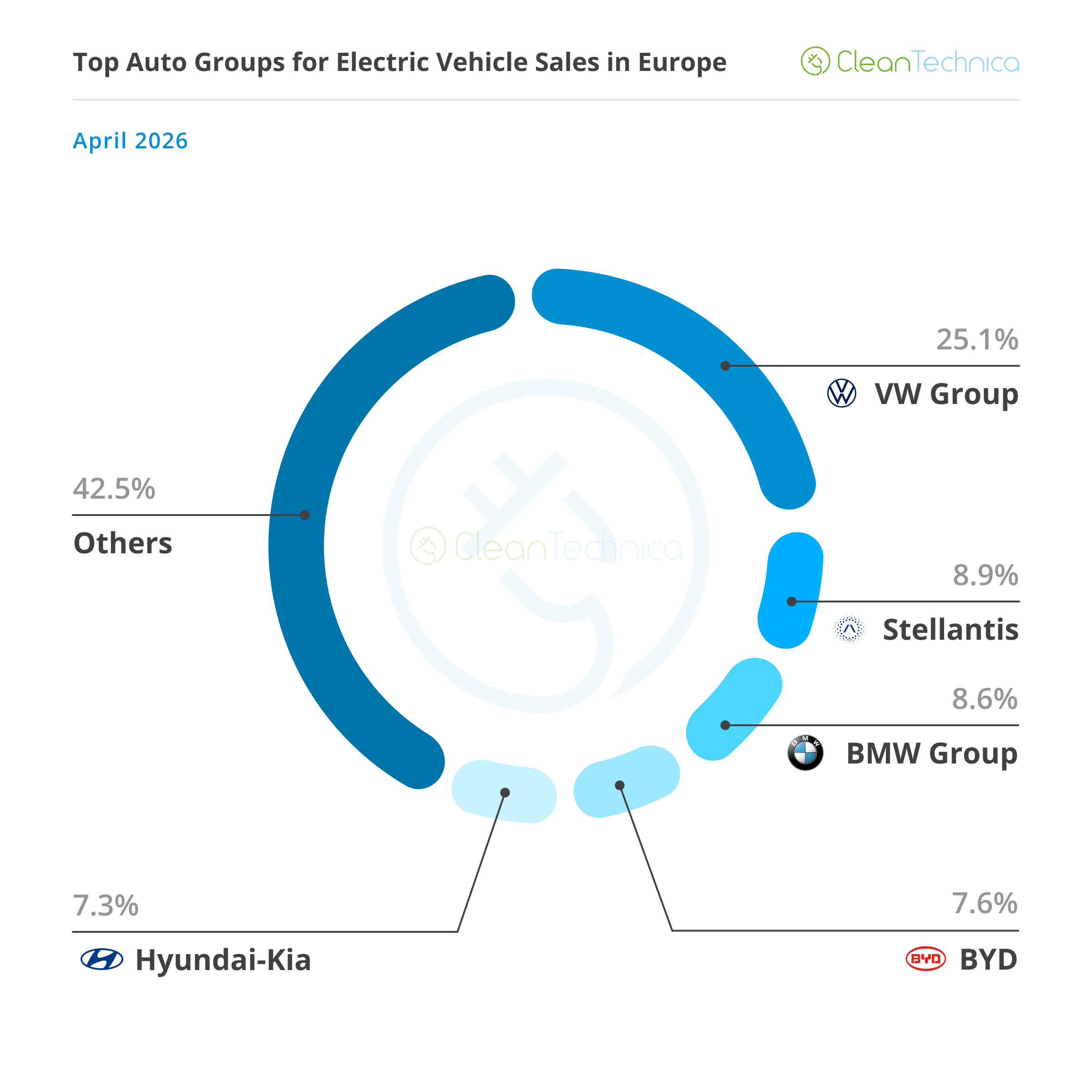

Arranging things by automotive group, Volkswagen Group is firmly in the lead, now at 25.1% share, a market share that is comparable to BYD’s in China and Tesla’s in the USA. This is an important metric for the German conglomerate if it wants to stay relevant in a fully electrified global automotive market. If you can’t win at home….

#2 Stellantis was down. Again. It now has 8.9% share. While the multinational OEM’s drop seems to have no end in sight, #3 BMW Group was up (8.6% now vs. 8.4% in March), and with the new iX3 surely adding significant volume to the tally in the near future, BMW should surpass Stellantis, maybe as soon as May.

Rising BYD (7.6%, up 0.3%) is still in 4th place, but if things continue as they are, I wouldn’t be surprised if we were to see the Shenzhen OEM in the runner-up spot at the end of the year.

Outside the top 5, Geely (6.6%, up from 6.5% in March) replaced Tesla in 6th, but for the time being, it does not have enough momentum to attempt a top 5 position.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy