Support CleanTechnica’s work through a Substack subscription or on Stripe.

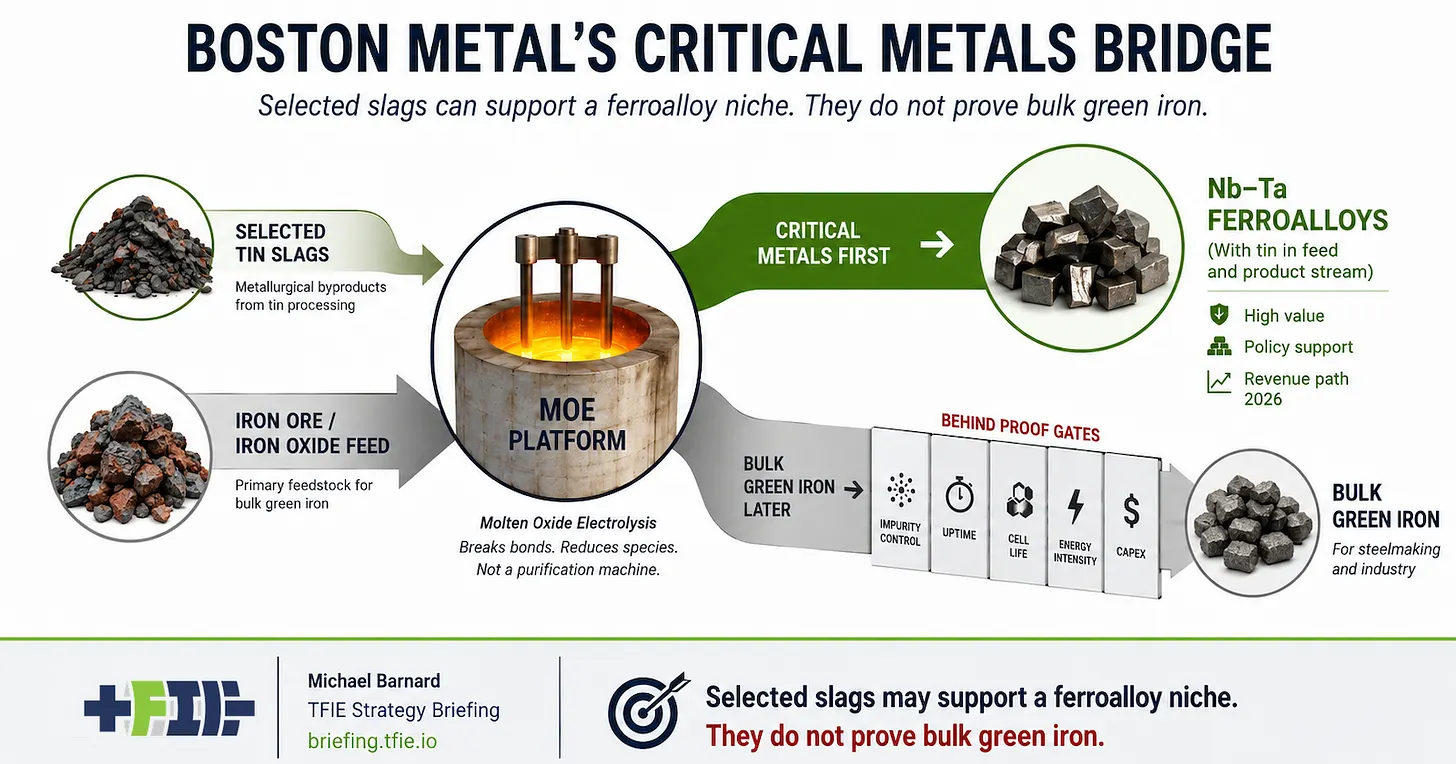

Boston Metal’s public story has shifted in a way that makes the company more credible in the near term, but less sweeping as a green-steel story. The company is still built around molten oxide electrolysis, or MOE, an electrically driven process for reducing metal oxides without coal. The near-term commercial evidence now points more strongly toward selected critical-metals recovery from suitable slags than toward bulk green iron.

That distinction is important because the public mental model for Boston Metal is still shaped by green steel. MOE is an elegant idea in that context. Use electricity, reduce metal oxides directly, produce oxygen instead of carbon dioxide and avoid the coal-based chemistry that dominates today’s primary steelmaking. As an industrial decarbonization concept, it is worth taking seriously, and it remains one of the more interesting approaches in the long list of pathways competing to clean up primary iron.

Steel, however, is not a forgiving market. Commodity iron has to be produced at enormous scale with high uptime, long cell life, stable feedstock behaviour, durable refractory systems, manageable anodes, competitive energy intensity, bankable capex and customers willing to qualify the product. It is not enough for the chemistry to work in a cell. The equipment has to become normal industrial plant, and it has to do so inside the brutal cost structure of a commodity market.

The critical-metals pathway has a different burden. Boston Metal’s current public direction points toward processing selected tin slags into ferroalloys involving niobium, tantalum and tin. That is a narrower market, but it is also a more plausible first commercial target. Specialty metals can support higher process costs than commodity iron, and enriched slag streams can contain enough value to justify additional processing if the recovery, energy use and product quality hold up.

That does not make the business easy. It changes the test. The cell is not the refinery. It reduces species according to the chemistry of the melt, and impurities can reduce along with the target metals if the feedstock and operating conditions allow it. Product quality, recovery rate, energy intensity, residue handling, campaign length, maintenance burden and customer qualification still determine whether contained value turns into recoverable margin.

This is where many “metals from waste” stories fail. The resource can be real, the metal can be valuable and the pitch can still be weak if the material is inconsistent, impurity control is poor, recovery is low, energy use is high or the output is hard to sell. Boston Metal’s version appears stronger than the generic version because tin-processing slags can be materially enriched in niobium and tantalum, and ferroalloy products are a coherent target. Stronger, however, is not the same thing as commercially proven.

The cleanest investor interpretation is that Boston Metal should be read first as a critical-metals recovery company with green iron as longer-dated option value. That may still be attractive. A viable specialty-metals business could generate revenue, preserve the technical team, deepen cell and anode learning, and give the company a more defensible operating base than a long wait for green steel. But the near-term diligence should focus on Brazil operations, feedstock rights, product qualification, customers, recovery rates, power costs, uptime, maintenance, residues and runway.

Steelmakers should keep watching MOE, but they should not treat critical-metals progress as procurement-grade evidence for green iron. Ironmaking has its own comparator set, and it is not standing still. Electric arc furnaces already dominate recycled steel and continue to improve as grids decarbonize. Hydrogen DRI, biomethane DRI, molten oxide electrolysis, flash ironmaking and other routes are competing for different parts of the future primary iron market. Boston Metal has to prove that its version is not merely clean, but industrially and economically better in the contexts where it wants to compete.

Policymakers should be equally careful. Critical minerals language can make weak evidence sound strategic, especially when supply-chain anxiety is high. Public support should be tied to demonstrated recovery, domestic or allied supply-chain value, environmental performance, residue handling and transparent operating data. A project can be strategically useful without being a broad green-steel solution, and funding decisions should not blur those categories.

Boston Metal has not failed. The company appears to have moved the first commercial burden to a market where unit value, policy interest and investor patience are more forgiving than bulk steel. That is a sensible industrial move if the process performs. It keeps MOE in the game and may produce useful critical-metals capacity, especially if the company can turn selected slags into repeatable ferroalloy products with reliable customers and transparent operating evidence.

What it does not do is prove that green steel has arrived. The right read is more disciplined: critical-metals recovery is the current evidence file, and green iron remains a separate proof burden. That framing is less exciting than the original green-steel narrative, but it is more useful for investors, steelmakers and policymakers trying to separate a credible first market from a fully validated industrial transition pathway.

Read the full TFIE Strategy Briefing assessment for the scorecard, evidence map, comparator analysis and update triggers.

https://briefing.tfie.io/p/boston-metal-moe-critical-metals-green-iron

Subscribe for decision-grade climate-tech diligence, not hype-cycle summaries.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy