Support CleanTechnica’s work through a Substack subscription or on Stripe.

BEVs on the way up, PHEVs on the way down

Plugin vehicle registrations were up 4% year over year (YoY) in May, ending the month at around 1.7 million units. Interestingly, BEVs (+15% YoY) and PHEVs (-15% YoY) had opposite performances, with pure electrics firm in double-digit growth while plugin hybrids remained in the red. This is the first time since 2019 that PHEVs remained in the red for five consecutive months.

This meant that, while the plugin YTD numbers are barely positive (+2% YoY), that is solely due to the PHEV blues (-11% YoY). BEVs are on their way back to normal (+9%).

And the different dynamics between pure electrics and plugin hybrids are reflected in the BEV vs. PHEV share of plugin sales — in May, BEVs represented 71% of all plugin sales, or about 1.2 million units, one of the best results of the past few years. That led the YTD breakdown to be 70% vs. 30% in favour of pure electrics, which is touching the ceiling of BEV share of the past 12 years. Since 2014, BEVs have floated between 70% and 50% of the total plugin share.

The global BEV takeover vs. China and the USA

The end of US incentives last October, added to the partial removal of incentives in China at the end of 2025, had an expected impact, meaning that these markets, the 3rd and 1st largest EV markets in the world, respectively, are dragging down global sales.

If we remove China and the USA from the tally, EVs jumped 39% YoY globally in May, with BEVs surging +47% YoY.

Funny enough, PHEVs are also underperforming in this metric, as the 20% PHEV growth rate in May, excluding China and the USA, is the lowest for the technology in over a year. It is starting to look like PHEVs’ current slowdown is more structural than expected.

Share-wise, May saw BEVs end the month at 19% share, with the tally increasing to 26% if we add in PHEVs. This performance pushed the 2026 plugin share upward. BEVs increased their share by one point, to 16%, while plugin hybrids remained at 6% share. Therefore, the 2026 PEV share is now at 22%.

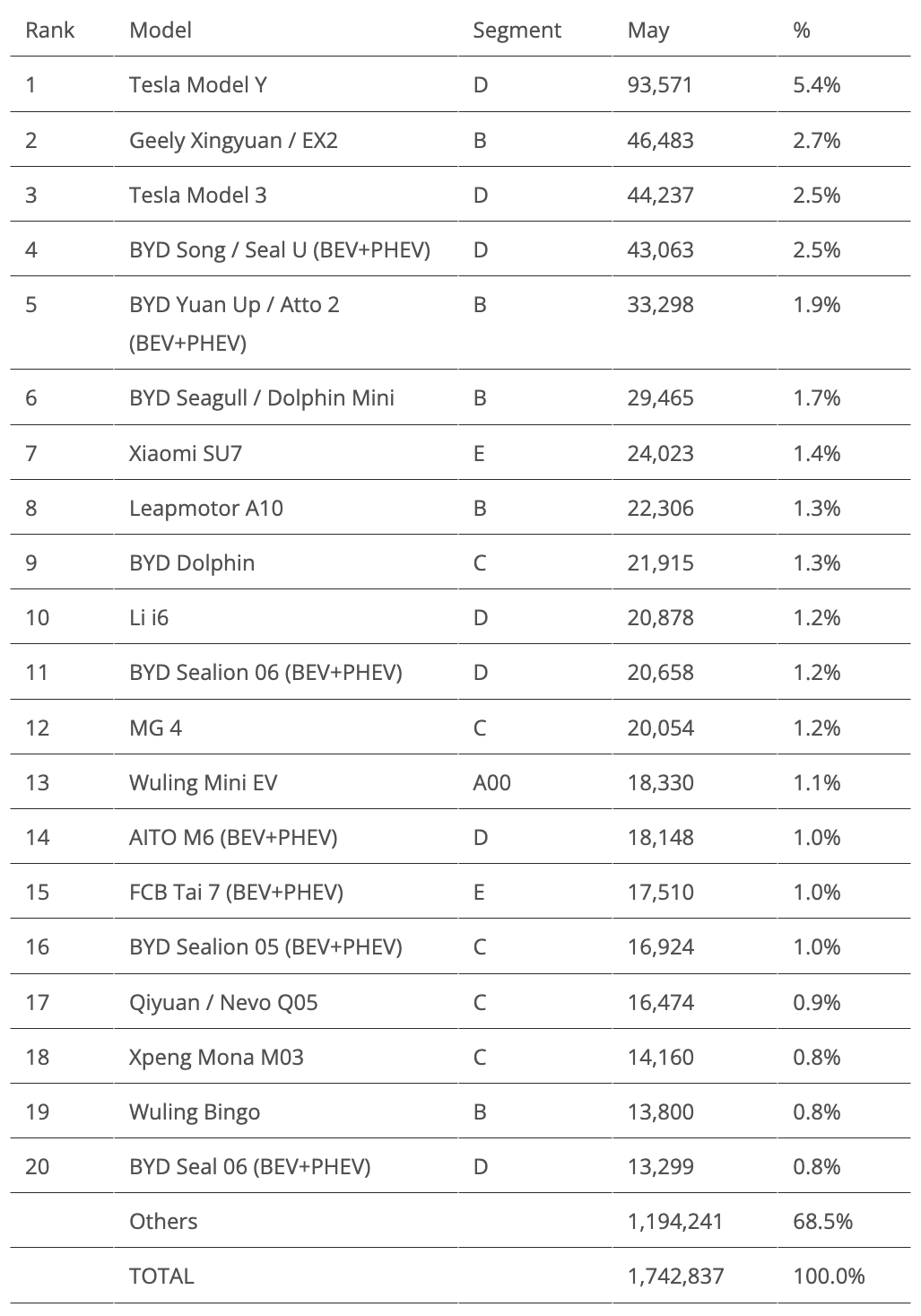

Looking at the best selling models, one can see that the Chinese market is recovering fast. Once again, there were no legacy OEM representatives in the top 20, and the Tesla Model 3 (44,237 units, up 28% YoY) was up to 3rd.

Still, the leader remained the Tesla Model Y (93,571 units, up 16% YoY), which has found a renewed youth thanks to the standard versions and the L three-row body.

This was enough to keep the Chinese competition behind it, like the Geely Xingyuan (EX2 in export markets), which completed the podium with some 47,000 registrations, up 20% YoY, in no small part thanks to export markets. Geely’s small EV is now at cruising speed, compensating for the loss of demand in its domestic market with increased exports.

A surprise in the top half of the table was the 4th position of the BYD Song. Despite being down 18% YoY in May, its sales performances are no doubt rejuvenated by the new-generation Ultra body, as May’s 43,000 units represented a new year best for the midsize model. Flash charging capabilities promise to recharge the Song’s sales and make it a serious candidate for podium positions in the second half of the year.

Another surprise was the 5th position of the BYD Yuan Up/Atto 2. Thanks to a recent refresh and the launch of a new PHEV version, the Up is becoming a star player in the BYD lineup.

Another highlight in the first half of the table is the Leapmotor A10. The hot startup’s new baby, a fully electric small crossover, was 8th. It scored 22,000 registrations in only its third month on the market, which is already the best position ever for a model from the startup. That could mean that Leapmotor has found its star player, joining a lineup of consistent performers.

Looking at the second half of the table, there is plenty to talk about:

- MG placed its 4 hatchback in 12th, thanks to a record 20,054 deliveries. The new generation is building on the success of its predecessor, and could become a serious threat to the leadership of the BYD Dolphin in the compact category.

- Still on SAIC, the tiny Wuling Mini EV is slowly recovering, having recorded 18,330 deliveries, a new year best. That allowed it end in 13th.

- AITO has a new success on its hands, with the new M6 SUV replicating the winning formula (large, comfy SUVs) in the midsize category. It scored 18,000 deliveries in only its 3rd month on the market. Will it be top 10 material soon?

- Another record scorer was the #17 Qiyuan Q05, with Changan’s mainstream crossover delivering a best ever 16,474 units.

- Finally, we have a number of returns to the table, with the BYD Sealion 05 in 16th thanks to 17,000 units, its best score in 11 months; the Xpeng Mona M03 18th with 14,000 units, its best performance since last November; and the new-generation Wuling Bingo bringing the nameplate back to the table, this time in 19th thanks to 13,800 units, its best result in a year.

Outside the top 20, there wasn’t much to talk about, with the highlight being the fact that the best selling legacy model belonged to Toyota. The BZ4X registered 11,119 units, ahead of the BMW iX1/X1 PHEV twins (10,746 units) and the Hyundai IONIQ 5 (10,478 units). That was its first 5-digit score since last September, when the US subsidies for EVs were about to end. It looks like the price cuts have brought the career of the Korean midsizer back to life in the USA, as the 5,000 units registered there in May attest.

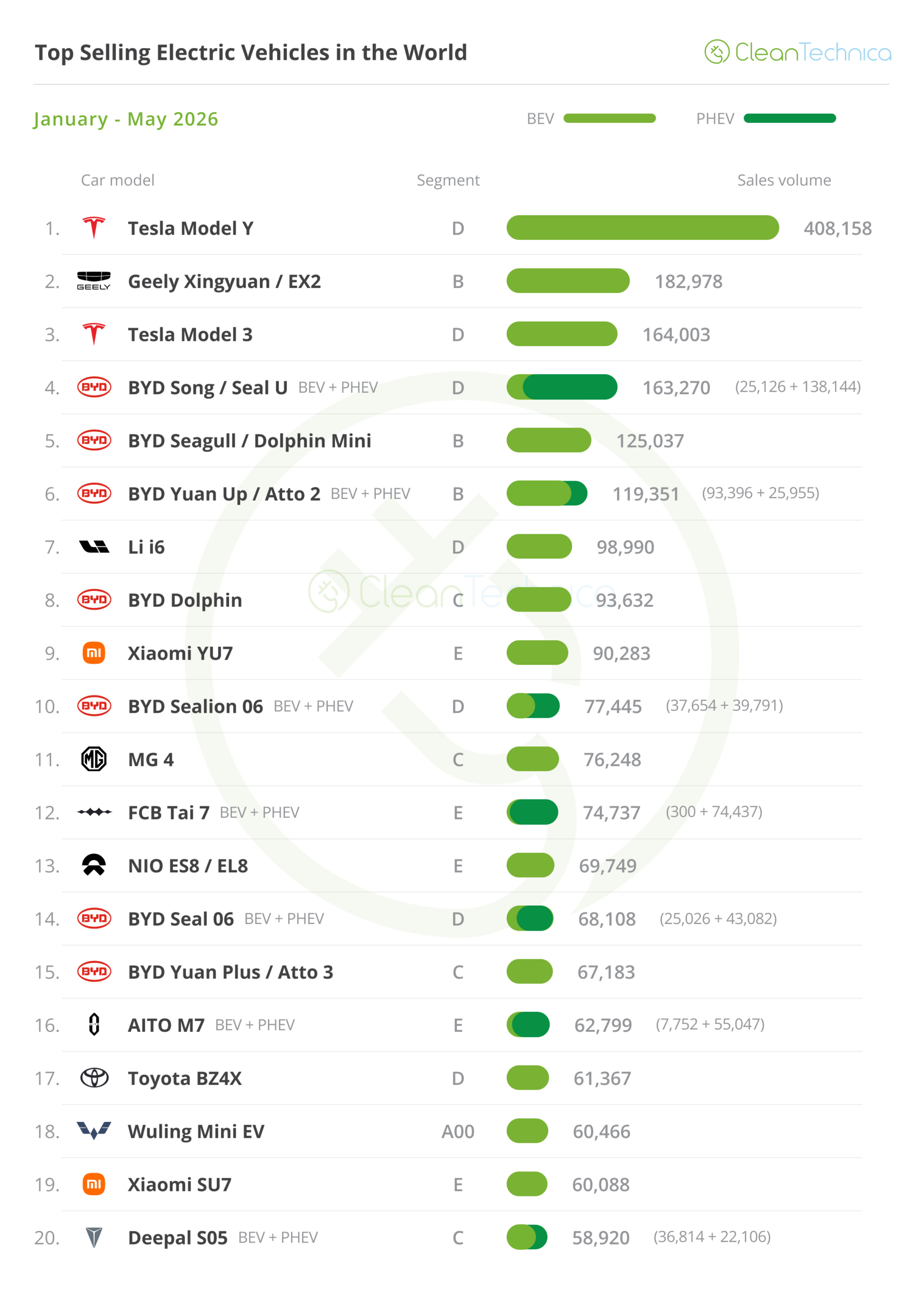

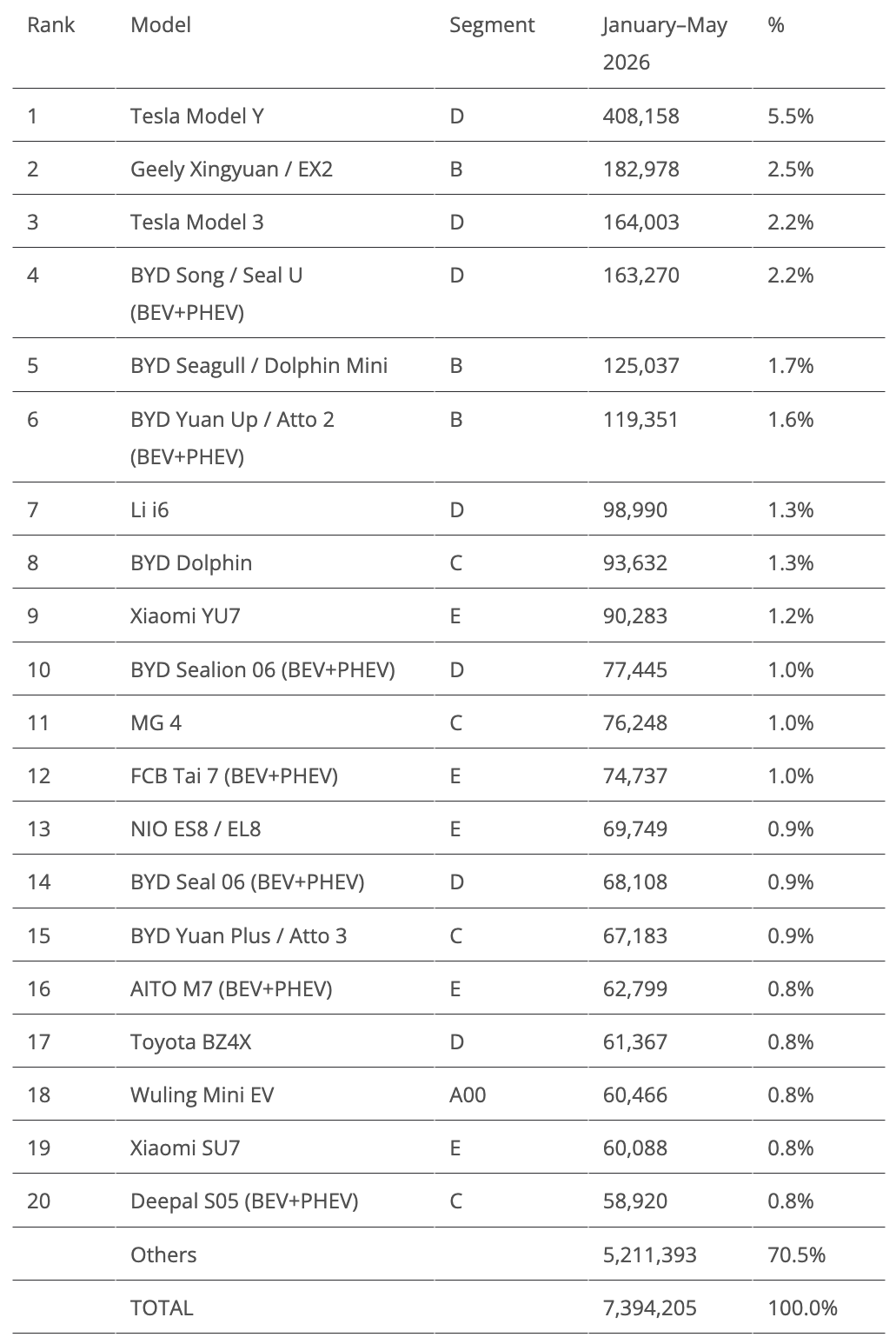

Year to date, the leader Tesla Model Y is really in its own league, selling twice as many units as the runner-up Geely Xingyuan.

Still on the podium, as expected, the Tesla Model 3 gained a bit more ground over the #4 BYD Song. Expect this distance to widen significantly in June as the Tesla sedan experiences its usual deliveries peak.

But with the Chinese SUV ramping up a new generation in China, and the current one still selling in volumes in export markets, it will be difficult for the Model 3 to retain a podium position, something it has held since 2018.

There were a couple more BYDs on the rise, with the Dolphin climbing one position to 8th while the BYD Sealion 06 jumped two positions to 10th, thus making it five BYDs in the top 10.

Elsewhere, the MG 4 compact hatchback continues on the rise, jumping two positions to #11, while we have two returns to the table — the tiny Wuling Mini EV showed up in 18th and the Xiaomi SU7 in 19th. This allowed Xiaomi’s two models to be present in the top 20, no small feat for such a new car brand.

Manufacturers: The Rise & Rise of Leapmotor

Nothing really out of the ordinary happened on the podium, with BYD, Tesla (+20% YoY), and Geely taking over the top three spots.

But behind these three, something remarkable has happened — Leapmotor scored another record result, with more than 81,000 registrations, ending May in 4th. It ended the month fewer than 9,000 units behind Geely. With a slew of fresh metal coming (A10 small crossover, A05 small hatchback, D19 large SUV, D99 large MPV…), expect the startup’s sales to continue growing significantly. So, Geely will have to watch out.

Another highlight was Zeekr, which ended the month in 10th with a record 34,377 registrations, all thanks to the success of its full size 9X and 8X large SUVs, which together had 15,000 registrations. There’s also the success of the 7X midsizer — thanks to export markets, it has seen its sales increase to 6,700 units.

Regarding the remaining positions on the table, another surprise was the record score of Changan’s Qiyuan, which delivered a record 29,264 units. That put it in the #20 spot. Its success was especially thanks to the success of its compact crossover, the Q05.

Finally, a reference is due for Hyundai, in 17th, with 31,000 registrations. It was its best score since last September, with the IONIQ 5 being the brand’s highlight.

Leapmotor surpasses Volkswagen

As for the year-to-date table, there was no major news on the podium, but right below it, things are changing.

Leapmotor is now … 4th. Bye bye, BMW. So long, Volkswagen. A Chinese startup has just surpassed you.

And while this is no major drama for BMW — after all, being this high up in the ranking is an anomaly, considering that the Bavarian OEM is only 13th in the overall automotive ranking. The same can’t be said about Volkswagen. No wonder they are now taking drastic measures….

Another Chinese brand going up is Wuling. It climbed to 6th thanks to the new-generation Bingo and the recovery of the Mini EV. I wouldn’t be surprised to see it also soon surpass Volkswagen….

Looking at the second half of the table, Xiaomi was up one spot, to 11th, having surpassed Mercedes. So, a two-year-old brand, which is part of a smartphone portfolio, has outsold the oldest carmaker in the world.

Final mentions go to Hyundai, which was up to 16th thanks to strong sales of the IONIQ 5 in the USA, and #18 AITO, which is now riding the wave of its new M6 model.

Looking at OEMs, BYD (19%) is stable in the lead, while runner-up Geely (10.1%) has benefitted from the good results of Zeekr and its namesake brand.

#3 Tesla (8.1%, up from 8% in April) stayed ahead of Volkswagen Group (7.6%), so it seems that the OEM is guaranteed a podium position this year.

#5 SAIC remained in 5th, with 6.6% share, while Hyundai–Kia (4.2%) is the new 6th placed OEM, having surpassed Chery (4.1%).

#8 Changan (3.9%) is now seeing a rising Leapmotor (9th, 3.6% share) getting close, so we might see a position change here, and Toyota is also starting to appear on the radar, with the Japanese OEM now in 11th with 2.8% share.

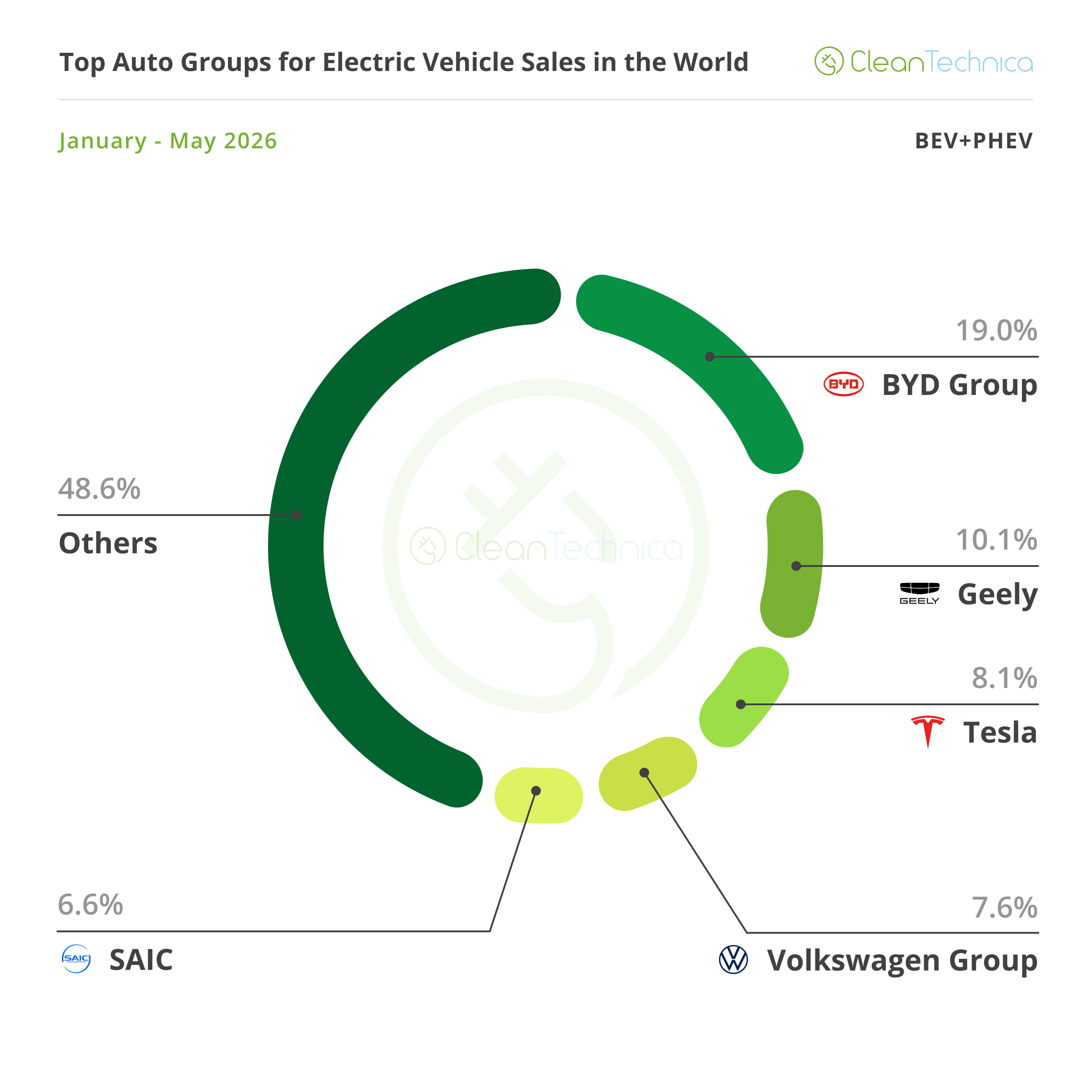

Looking just at BEVs, there were about 5.2 million registrations so far this year, or 70% of total plugin sales. Will they end the year above 75%? If so, that would be their best result since 2012....

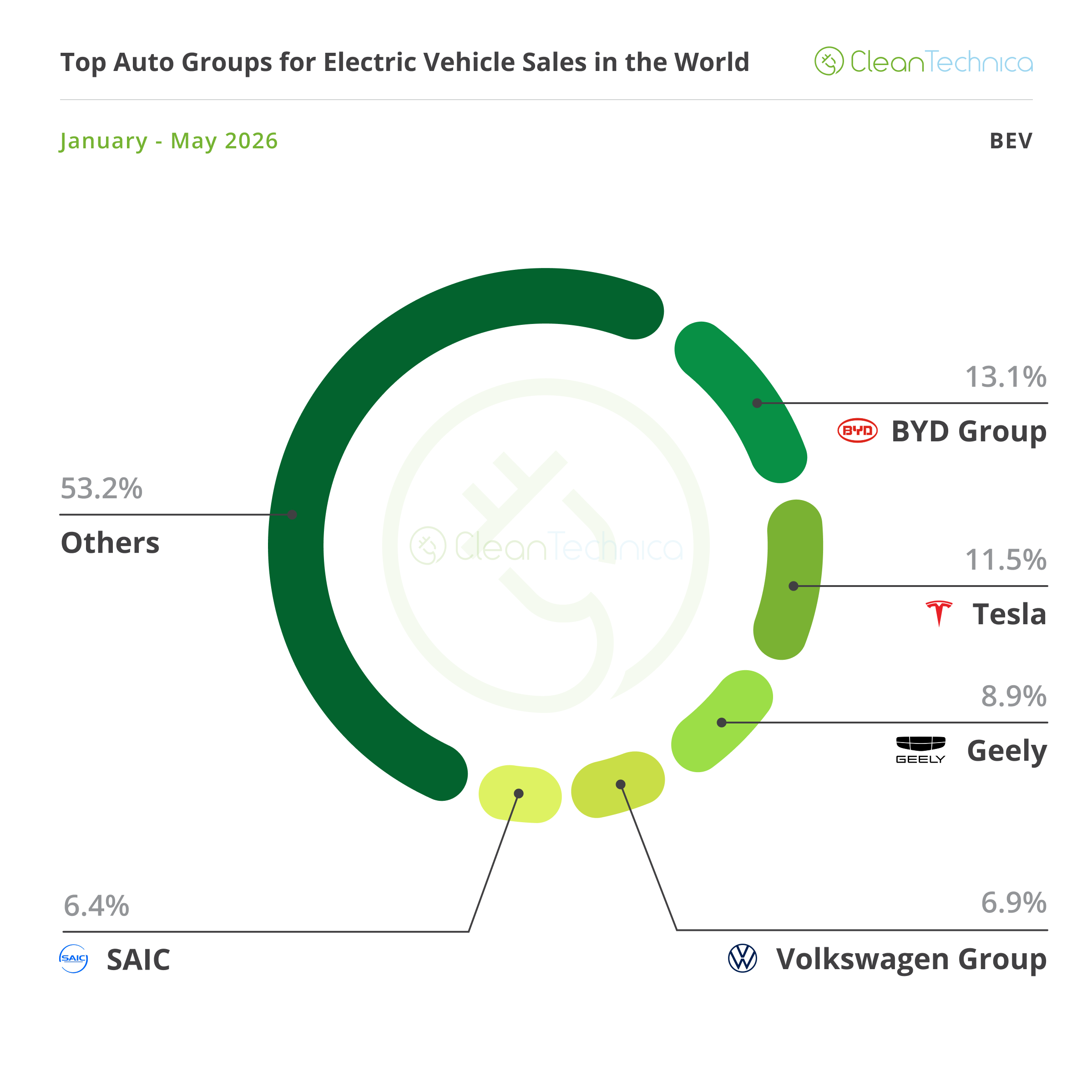

At the top, Tesla (11.5%) is stable in the runner-up spot, while leader BYD (13.1%) seems to have gained enough advantage to keep Tesla at bay (the Texan will have its usual peak month in June).

In 3rd place, we have Geely (8.9%), keeping #4 Volkswagen Group at bay (6.9%, down 0.1% share). Meanwhile, #5 SAIC (6.4%, up from 6.3% in April) is starting to reach the back of the German OEM.

Outside the top 5, #6 Hyundai–Kia (4.8% share) is the only OEM close to the top 5 makers.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy