Europe EV Sales Report — The King (Tesla) is Dead, Long Live the (Old) King, Volkswagen

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and/or follow us on Google News!

Last Updated on: 2nd May 2025, 02:25 am

It was the second best month ever in Europe.

Some 365,000 plugin vehicles were registered in Europe in March, rising 22% year over year (YoY), which is a particularly positive sign when considering that the overall market was up by just 3% in the same month, to some 1.4 million units.

Interestingly, BEVs are the ones pushing the market upwards, growing 24% YoY in March to 245,000 units, their second best month ever (only behind December 2022).

Talking about PHEVs, there’s also good news here, as they left negative numbers and grew 19% in March, their highest growth rate since January 2024. They are now close to 120,000 units. This is their second highest score ever as well, only behind December 2022. Their YTD numbers are now back in black, now up 6% to 270,000 units.

As such, March saw the plugin vehicle share of the overall European auto market grow to 26% (17% full electrics/BEVs), one percent above the year-to-date numbers.

These results moved the 2025 BEV/PHEV share breakdown to 68% vs. 32%, meaning that plugin hybrids recovered one percent share, and the 2025 score is now closer to the final result of 2024, 67% for BEVs and 33% for PHEVs.

Finally, looking at the sales breakdown between the remaining powertrains, besides the usual steep fall of diesel sales, down 27% YoY to 7% share now, petrol is also in a death spiral. Petrol vehicles saw their sales fall by 20% YoY, and their share dropped to 28%.

Besides plugins, the other current major winner is plugless hybrids, with HEV sales jumping 25% YoY to 37% share. That’s a significant increase over the 31% HEVs had 12 months ago. This means that 63% of all car sales in Europe in February had some kind of electrification.

With these numbers in mind, one can say that diesel sales should effectively be dead in about three years time, while petrol should share the same fate a few years later (2031? 2032?), which will mean that by 2032, the whole European market will be at least partially electrified.

The EU target is for there to be only zero-emission vehicles by 2035 — i.e., only BEVs (FCEVs and synthetic fuels will remain a small niche). Will the market be ready for it? What do you think?

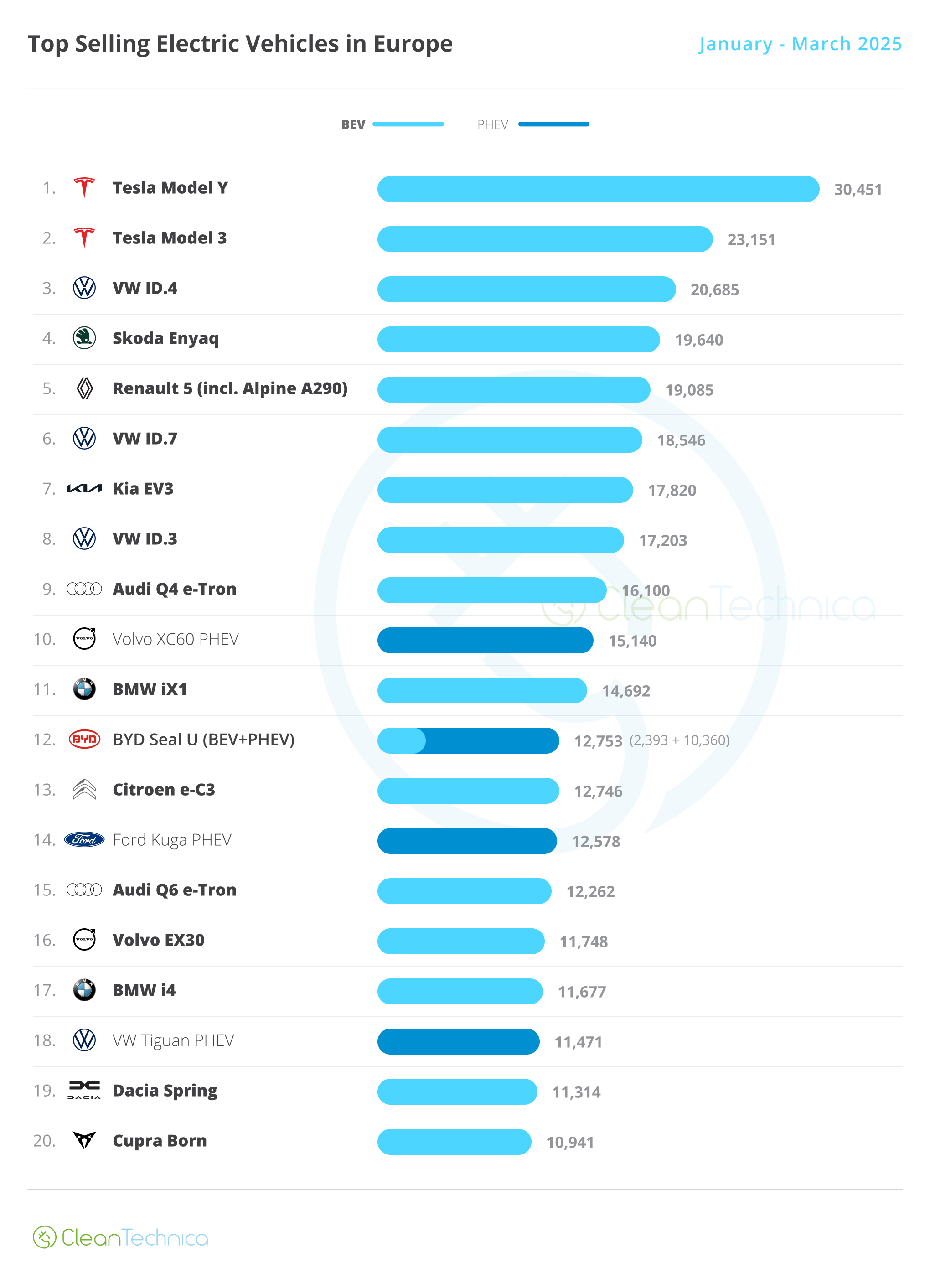

But let’s get back to March’s sales, the highlights this month were Tesla winning 1st and 2nd and the Renault 5 winning its second bronze medal in a row. Here’s a more detailed analysis on the top 5 EVs this month:

#1 Tesla Model Y — Tesla’s crossover once again won the monthly best seller title, thanks to 15,707 registrations. Still, when we compare with the same month last year, deliveries were down by an astounding 41% YoY, almost half of the sales of March 2024. Remember when I mentioned that 2023/24 would be considered the “peak Model Y” period in Europe? Tesla’s midsizer has hit the market’s natural limits. Sure, the refreshed Model Y version could help things along in Q2, but on the other hand, the name Tesla has become toxic for many, limiting its appeal, so don’t expect the Model Y’s performance to go back to the sky high results it once had. Expect the leader of the European EV market to stay on top in the foreseeable future, but with ever smaller winning margins and the occasional loss, especially in the first months of each quarter.

#2 Tesla Model 3 — The China-made (but with a US passport) sedan scored 12,554 registrations in March. That represented 6% growth YoY, but looking at the whole quarter, deliveries were down by 14%. The explanations for this slowdown amount to three things: First are the China tariffs, which have somewhat hurt the sedan’s performance. (The reason why Tesla hasn’t started to make it in Germany is beyond me.) The second reason has to do with increased competition, like the VW ID.7, which has experienced an exponential surge in sales this year, ending March in 6th and maybe giving the Model 3 a run for its money in the 2025 race. Thirdly, Musk’s political shenanigans have started to take a toll on European buyers. I would say it affects some 10–15% of Tesla’s total sales, meaning that it might affect those who were on the fence between buying a Tesla or another brand as well as those who are more politically motivated. Still, we are only three months into the new US presidency, so who knows how much more damage the Tesla brand will face five months from now?

#3 Renault 5/Alpine A290 — Renault’s new star player delivered 8,047 units (with the help of its sportier Alpine twin), a new record result for the French model and its second podium presence in a row. The perky French hatch could aspire to go even higher up in April, especially profiting from Tesla’s off-peak month. With silver looking likely, it won’t be completely impossible to see the Renault EV beat the Model Y…. While the Renault 5 isn’t class-leading specs-wise and it has too many command stalks, it more than compensates for that in character, be it regarding the eye-catching design or the fun-loving driving dynamics. Together with correct prices and range, those things make it a very compelling offer for European buyers. One can even say that it is a car developed and built for the European mindset.

#4 Skoda Enyaq — Despite the internal competition of the recently introduced Elroq (17th in March, with a record 4,595 units), Skoda’s original electric crossover is still going strong, scoring 7,629 registrations in March, almost doubling its sales YoY. With the younger, cheaper Elroq now stealing part of its spotlight, one has to recognize the resilience of the Enyaq and its ability to remain top 5 material. If the Enyaq stays at around 6,000 to 7,000 units per month, even with the Elroq fully ramped up — at, say, 7,000 units — this will allow a significant 14,000 BEVs every month for the Czech brand, which would leave Skoda managers (and the head honchos in Wolfsburg) very happy indeed.

#5 Volkswagen ID.4 — The compact crossover won another top 5 presence in March, with the MEB-platform model scoring 7,594 deliveries, meaning 52% growth YoY and its best score in 17 months! This also allowed Volkswagen Group to place two models on the best sellers table (as the Skoda Enyaq took the 4th spot). With improved specs and lower prices (and the small detail that Volkswagen Group needs to sell more BEVs to keep up with the EU’s CO2 rules…), the German crossover is experiencing a second youth. While not EV enthusiasts’ choice, the ID.4 has enough going for it to attract a wide audience.

Looking at the rest of the March table, and considering that this was the second best month ever for electric vehicles, record scores were aplenty. Volkswagen Group in particular posting a strong collective result, with four models (#6 VW ID.7, #14 Audi Q6 e-tron, #15 VW Tiguan PHEV, and #17 Skoda Elroq) placing best ever scores.

The ID.7 record is particularly interesting in the context of a troubled Tesla, as the big VW seems to be a direct beneficiary of the US brand’s sales blues in Europe.

More proof of Volkswagen Group’s current strength in Europe is the fact that it placed eight models in the top 20…. Kind of reminds me of a certain Shenzhen-based OEM in the Chinese market.

But other models outside the Volkswagen Galaxy also scored record results, like the #7 Kia EV3, building upon the success of its Kia Niro EV predecessor. It had some 7,000 registrations. Meanwhile, the #18 Renault Scenic crossover gave Renault a second record score in March (4,429 units) — along with the third-placed Renault 5’s/Alpine A290’s record score — proving that the French carmaker is back in the game.

Another brand with positive numbers is BMW. The German carmaker placed its iX1 compact crossover in 10th with 6,343 units, its best score since 2023. Additionally, the i4 midsize sedan fastback was 15th, with 5,033 units, its best score in a year.

But the most important highlight of this month was the amazing score of the #8 BYD Seal U, the euro-spec version of the BYD Song. With close to 7,000 units in just one month, it is the best result ever for a BYD model in Europe — by some distance — and the vast majority of them (some 6,000 units) belong to the PHEV version, as that version benefits from lower tariffs (the standard 10%) compared to its BEV siblings. As such, it is not surprising that several Chinese OEMs — like Chery, Geely, and BYD — are introducing new PHEV models to Europe. They are all probably looking to replicate the success of the Song PHEV — I mean, Seal U PHEV, in Europe.

Another interesting aspect of the recent Seal U success in Europe is that it is happening at the same time that its donor model, the Song, is starting to lose ground in its domestic market, with local buyers now preferring other BYD models, like the Song L, that are newer and more attractive.

And the BYD success in Europe does not come exclusively from the Seal U, as the Seal midsize sedan also hit a record score, 2,706 units. Additionally, the recently launched Sea Lion 07, a posh midsize SUV-coupe, is ramping up, having scored 1,671 units in March. That means that BYD sold over 11,000 midsize units in March alone!

I guess the Shenzhen make is another brand benefitting from defecting Tesla buyers….

Outside the top 20, it wasn’t only the BYD models shining, as there were several other record results on the table. For example, there’s the case of the funky Toyota C-HR PHEV (4,014 units), and the bug-eyed Hyundai Inster (2,559 units). BMW also had reasons to celebrate, as the iX2 sporty crossover scored 2,733 units and the i5 full size model hit a best ever 2,966 units, which would usually grant it the lead in the category, but…

… It didn’t, because the new Audi A6 e-tron production ramp-up allowed it to reach a record high of 3,136 units. So, the big Audi took the category title. With class-leading specs (700 km-plus ranges + 270 kW charging speed) and reasonable pricing in a no-nonsense body (and station wagon — Avant — versions!), this is the recipe for success that the German premium makes need to follow. The badge alone won’t grant them success anymore. They need to work for it.

But it wasn’t only the A6 e-tron shining in the VW stable, as the sporty Cupra Tavascan continued to ramp up deliveries, reaching 3,272 units, while the charismatic ID. BUZZ is benefitting from the 7-seat version and also ramping up deliveries, now at 2,722 units.

The German brand should have launched the 7-seat version sooner — I mean, it doesn’t make any sense to launch a midsize MPV as a 5-seater only, does it? It’s almost like they didn’t want it to sell in large numbers….

Finally, a mention for the Polestar 4, which hit a record 2,239 units. It beat the aging (but cheaper) Polestar 2, thus becoming the best seller of the brand. It seems that the lack of a rear window isn’t a major deterrent to the success of the Polestar’s … thingy (crossover? fastback in heels? something else?). Good news for the Sino-Swede, and we all know they are in need of that….

Looking at the 2025 ranking, the big news is the return of the Tesla Model 3 to the runner-up position, jumping six positions and displacing the VW ID.4 from the runner-up position.

So, with Teslas back at the top and two Volkswagen Group models competing for 3rd, it’s 2024 (and 2023, and 2022…) all over again, right?

Well … not quite.

The leader, the Tesla Model Y, is down an astounding 48% YoYÂ and is now #34 in the overall market, miles away from the top 5 positions it navigated last year.

So, yes, it is still leading, but this year the US crossover should not take the Best Seller title for granted — which would be its 4th in a row — especially if Tesla’s reputation continues to be tarnished on a daily basis….

As for the Tesla Model 3, thanks to the expected delivery peak in March, it is back at its usual 2nd position, but with sales down 14% YoY and not the rosiest of outlooks for the remainder of the year (the Model Y refresh should steal some of its sales and the Tesla branding is increasingly toxic), the ones behind it will have a shot at surpassing it.

And there are quite a few that could do it…. There are four models within 5,000 units of the Model 3, including the VW ID.7, which is a direct competitor.

Which leads us to the Model 3 chasers: three models from Volkswagen Group (#3 VW ID.4, #4 Skoda Enyaq, and #6 VW ID.7) and the child genius Renault 5.

The most likely competitors for the Tesla sedan will be the VW ID.4 and the French hatchback, as the Skoda Enyaq now will have to split the stage with its smaller Elroq sibling and the VW ID.7 is simply too expensive (prices starting from 55,000 euros) to have a chance to fight for a podium position.

With the Renault EV winning two consecutive Best Selling Non-Tesla prizes, I would say that the French model will be the main beneficiary from a Model 3 fall from grace. Of course, Volkswagen could always pre-register a boatload of ID.4’s in December in order to avoid CO2-related fines and push its crossover to unexpected heights….

One thing is certain: for the first time in years, the race for second place will be an interesting one.

Another highlight was the rise of BMW’s dynamic duo, with the iX1 climbing to #11 and the i4 to #17. Additionally, the recently introduced Audi Q6 e-tron jumped five positions, to #15.

Which sounds impressive, until we realise that the BYD Seal U joined the table in … #12!

With competitive pricing (40,000 EUR for the PHEV, 43,000 EUR for the BEV), BYD’s midsize SUV is an everything-killer, and it’s not a coincidence that the midsize category leaders (Tesla Model Y in the BEV section, Volvo XC60 among PHEVs) are facing stagnating or falling sales in a growing market.

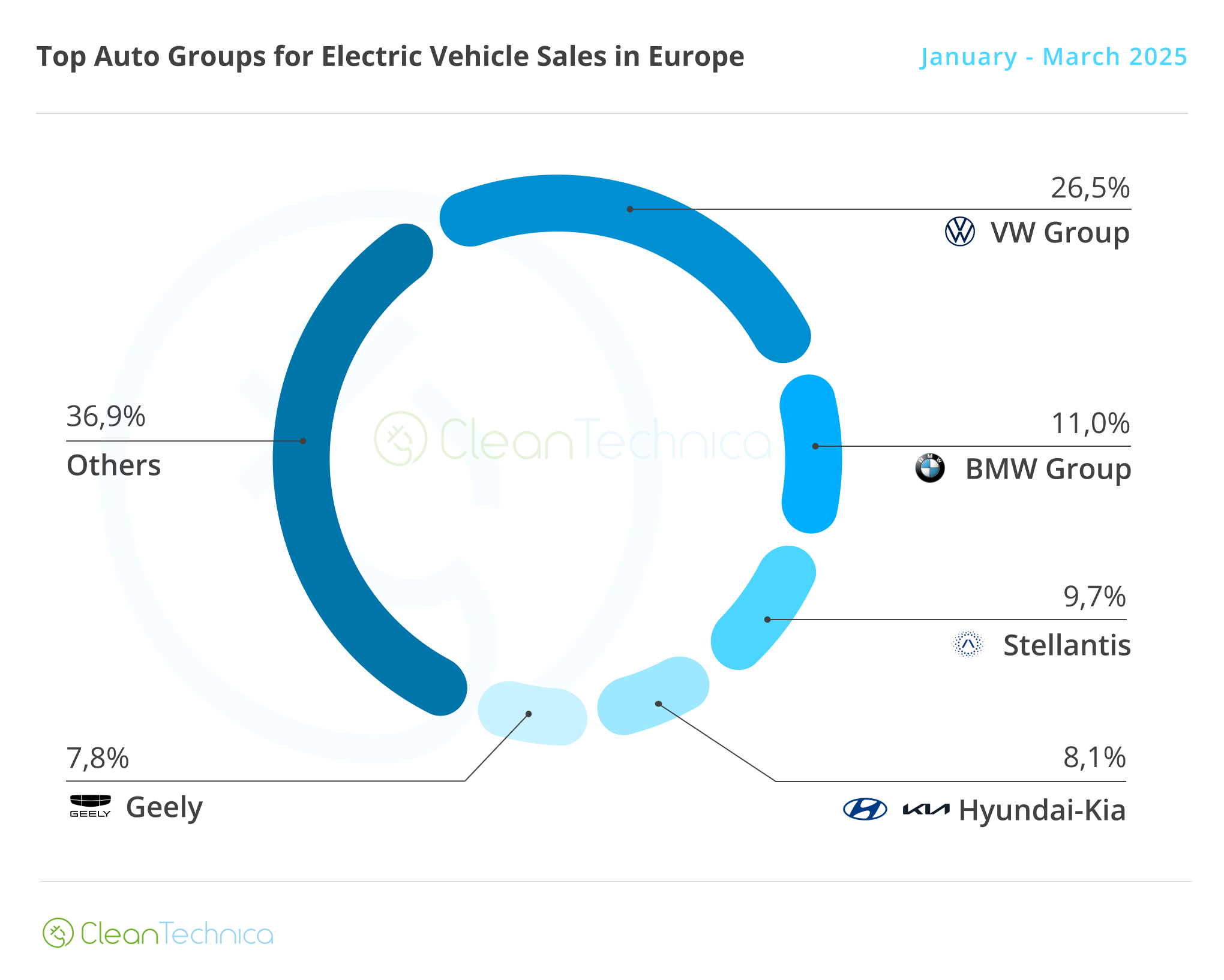

As for the plugin auto brand ranking, Tesla benefitted from its peak month and recovered share (6.4% in March vs. 5.3% in February), but it was too far behind #1 Volkswagen (10.8%, down 0.4% in March), #2 BMW (9.3%, down from 9.5% in February), or even #3 Mercedes (7.1%, down 0.1% in March) to reach podium status. The US make only managed to surpass Volvo (5.9%, down from 6.3% in February), and is now in 5th.

And this already accounts with a full quarter, so this is an end of an era in the European plugin market. After three years of full Tesla domination, the best that the US make can hope is to surpass Mercedes and reach the podium.

The best seller title should then change to the previous owner, Volkswagen, winner in 2015, 2020, and 2021. Should VW win the 2025 title, it would then equal Tesla in the number of European manufacturer titles, with the Texan brand having won in 2019, 2022, 2023 and 2024.

Tesla’s current woes in Europe are not just branding issues, even though as I have said previously, they are significant.

It runs deeper than that.

Tesla was once seen as disruptor, the fresh new take on EVs and the automotive business, but that lasted until 2019/2020.

After that, Tesla stopped innovating and has been basically running on inertia and brand power. The thing is, both of these enablers are ending. Add in decent, and in many cases superior, competition, and now Tesla is looking like old news. Tesla has become a legacy OEM.

Have doubts? Just look at this, Tesla share in Europe:

- 2018 – 6.9%

- 2019 – 19.9%

- 2020 – 7.3%

- 2021 – 7%

- 2022 – 9%

- 2023 – 12.1%

- 2024 – 11%

- 2025 Q1 – 6.4%

We have to go back to 2013(!), when the Model S was starting out, to see Tesla with such a small share in Europe, 6.2% at the time. So … yes, the (Tesla) King is dead in Europe. And only a full reincarnation will resurrect it.

But I digress. Below the top 5, Renault (4.3%, up 0.1%) is continuing to grow, having shortened the distance to #7 Kia (4.6% in March, down from 4.8% in February) and #6 Audi (5.1%).

A last mention goes to BYD, which is already appearing on the radar with 3.5% share. That’s more than Ford and … Toyota!

Arranging things by automotive group, Volkswagen Group is firmly in the lead, with 26.5% share, a market share that is comparable to BYD’s in China and Tesla’s in the USA. This is an important metric for the German conglomerate if it wants to stay relevant in a fully electrified global automotive market.

If you can’t win at home….

BMW Group (11%, down from 11.3% in February) remained in the runner-up position in March, while #3 Stellantis is back in the losing share game (9.7% in March vs. 10.1% in February) thanks to the Citroen e-C3 EV failing to stabilize (it dropped to #20 in March) and the remaining lineup really not helping (the 2nd best seller was the six-year-old Peugeot e-208, with 2,814 registrations).

The problem for Stellantis is that just one model being sold in large volumes won’t be enough to keep a podium position. Just ask Tesla. It needs to ramp up production of its lower priced models (Fiat Grande Panda EV, Opel Frontera EV, Citroen e-C3 Aircross EV, etc.) sooner rather than later.

Hyundai–Kia (8.1%) remained in 4th. While #5 Geely (7.8%, down 0.5%) continued to slide, and the blame is not only on Volvo, because Lynk & Co is down 21% YoY while Smart is doing even worse, cratering 66% YoY…. These two brands need new models, and fast.

With the lonely Renault pulling deadweights (Nissan and Mitsubishi) on its back, do not expect the #7 Renault–Nissan Alliance (6.8%) to disturb the top 5. The same can be said about #6 Mercedes (7.1%) now that Smart has gone to Geely.

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy