Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and/or follow us on Google News!

Trump’s aggressive economic policies in Q1 2025 have triggered immediate ripples throughout global maritime logistics, reshaping shipping routes, port activity, fuel consumption, and emissions trajectories. I’ve been seeing statistics on container volumes and hearing from industry insiders that they are bracing for empty US ports in coming weeks. It’s time for another article on the theme of Trump: Inadvertent Climate Hero.

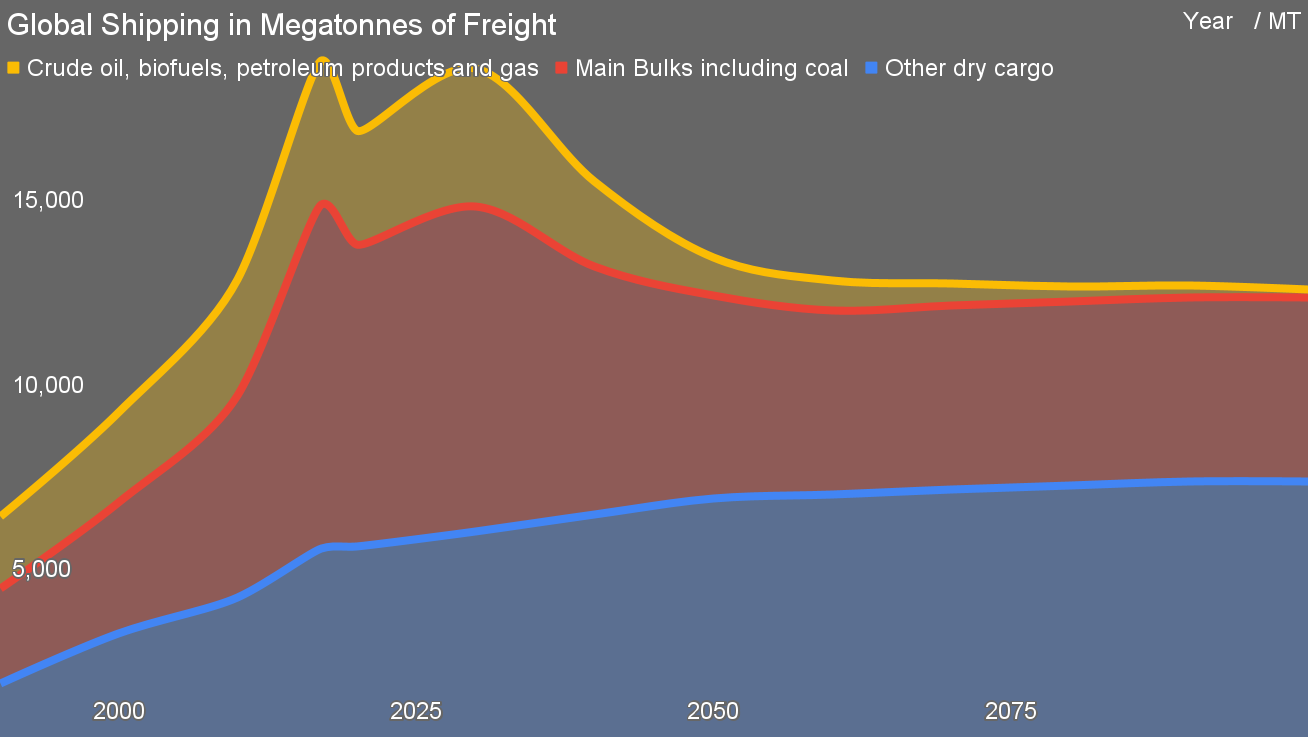

Three years ago, I published the first version of my maritime shipping decarbonization projection through 2100. It forecast a return to almost 2019 levels by 2025, then a gradual decline. A great deal of that was due to the slow reduction of bulk fossil fuel shipping, which accounts for 40% of all maritime tonnage. With peak oil, gas, and coal and the subsequent decline, along with alternative power of maritime shipping, including electrification of inland and nearshore shipping, along with increased efficiency measures, I projected a significant decline in total shipping tonnages. As a note, while the International Maritime Organization’s (IMO) modeling scenarios do include the impacts of reduced fossil fuel demand, they still project an increase in total shipping tonnage through 2050, something I consider highly unlikely.

I tend not to include short term politics in my long term projections, because blips tends to smooth out over time. However, Trump’s actions may be triggering a more rapid transition. To properly assess the scale and depth of this disruption, we need a clear baseline: the global maritime conditions of 2023, a year marked by relative stability despite lingering post-pandemic supply chain adjustments.

In 2023, global maritime trade had largely recovered from COVID-19 disruptions, with major ports such as Los Angeles, Shanghai, Rotterdam, and Singapore operating at near-full capacity. Container throughput remained robust, with trans-Pacific routes, especially from China to the U.S. West Coast, experiencing consistently high volumes. Maritime fuels in 2023 were dominated by very-low-sulfur fuel oil (VLSFO) due to the IMO‚Äôs stringent sulfur cap implemented in 2020, but heavy fuel oil (HFO) and liquefied natural gas (LNG) modest roles. According to IMO assessments, emissions from shipping, including carbon dioxide (CO‚āā), sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter (PM), showed incremental reductions due to improved fuel standards, vessel efficiency gains, and regulatory incentives for cleaner fuels.

Fast-forward to early 2025, and the immediate impacts of Trump’s renewed tariff regime have become starkly evident. The United States, the epicenter of tariff-related disruption, saw a dramatic reconfiguration in port activities. West Coast ports, traditionally the primary gateways for Asian imports, particularly from China, began experiencing significant volume drops. By March 2025, the Port of Los Angeles reported monthly container throughput down by nearly 6% compared to previous months. In contrast, East and Gulf Coast ports such as Norfolk and Houston benefited, with Norfolk reporting nearly a 28% volume increase during the same period. This eastward shift reflected logistical attempts by importers and shipping companies to circumvent tariff-related bottlenecks and uncertainties plaguing West Coast terminals.

On the other side of the Pacific, the impacts were equally pronounced, though economically inverse. Chinese ports, historically bustling hubs underpinning global trade networks, faced sudden declines in container traffic bound for the U.S. market. Preliminary port data for early 2025 indicated volumes dropping by as much as 17% year-over-year at major Chinese gateways. According to shipping consultancy Alphaliner, numerous scheduled sailings between China and U.S. ports were abruptly canceled, removing several hundred thousand containers from expected transport capacity. The effect cascaded through local economies, leading to reduced port staffing, idle cranes, and underutilized intermodal rail infrastructure.

As traditional routes between China and the United States faltered, shippers have been seeking alternative markets and intermediaries. Vietnam, a rising manufacturing power already benefiting from previous trade conflicts, witnessed sharp increases in shipping volumes as importers preemptively rerouted Chinese-origin goods through Vietnamese ports to minimize tariff impacts. According to Bloomberg reporting, freight rates for containers from Vietnam to North America spiked significantly, surpassing those from China by April 2025 ‚ÄĒ a remarkable market inversion. Similarly, Mexican ports like Manzanillo saw heightened activity, prompting announcements of accelerated investment in port expansions and infrastructure upgrades to accommodate a projected doubling in container throughput capacity. European ports observed a modest rise in container traffic, primarily due to Asian exporters redirecting excess capacity toward EU markets as an alternative to increasingly restricted U.S. entry points.

Operational adjustments among shipping lines compounded these geographical shifts. Blank sailings ‚ÄĒ cancelled voyages to balance vessel capacity with diminished demand ‚ÄĒ became a common strategic response, reaching unprecedented levels. Freightos reported that on some Asia‚ÄďU.S. routes, nearly half of scheduled voyages were canceled in April 2025 alone. Concurrently, carriers are increasing their reliance on longer alternative routes via the Panama Canal to access East Coast ports directly, indirectly lengthening voyages and slightly elevating fuel consumption per container shipped. Moreover, ports are facing paradoxical congestion spikes due to uneven cargo flows and displaced volumes, resulting in logistical inefficiencies that echoed the disruptive supply-chain bottlenecks previously experienced during the pandemic.

The immediate impact of these operational changes was reflected directly in marine fuel consumption patterns. Major bunkering hubs such as Singapore and Fujairah reported bunker fuel sales declining by approximately 9% in the first quarter of 2025 compared to the prior year, according to industry sources. This decline predominantly affected traditional marine fuels, particularly VLSFO and residual HFO. However, LNG fuel usage continued to grow, driven by new vessel deployments aligned with stricter EU emissions regulations (e.g., FuelEU Maritime and European Emissions Trading System), which came into force concurrently in January 2025.

Even amid declining overall fuel demand, LNG bunkering maintained an upward trajectory, indicating continued regulatory and market-driven momentum towards cleaner fuel options. That’s problematic, as the ICCT FUMES report made it clear that LNG slippage from maritime engines was about double what the industry had been using as an assumption, putting their actual CO2e emissions 20% to 30% above VLSFO, not 20% to 30% below it. Regardless, LNG is still a relatively small proportion of maritime fuels, dominantly in LNG tankers unsurprisingly, but also cruise ships and ferries, where passengers not being subject to VLSFO combustion smoke is a priority.

Correspondingly, emissions from maritime shipping began to see reductions consistent with decreased overall fuel consumption. Preliminary emissions data extrapolated from reduced fuel sales suggest measurable declines in CO‚āā, SOx, NOx, and particulate matter emissions in the first months of 2025. These emissions reductions were somewhat offset by increased distances traveled via alternative routes.

Shipping companies responded to these changing conditions with notable strategic realignments. Major carriers are accelerating the scrapping of older, less-efficient ships, and delaying or canceling deliveries of new tonnage to mitigate excess capacity. Investments continued, albeit more cautiously, focused primarily on fuel-efficient, dual-fuel LNG-capable vessels to comply with stringent environmental regulations and hedge against volatile fuel markets. Financial impacts for shipping firms were mixed; while volume declines pressured revenues, carriers are benefiting from temporarily lower operational costs due to reduced fuel expenses. Many shipping lines proactively engaged in hedging strategies for bunker fuels, emphasizing cost management to navigate uncertain demand forecasts.

Regulatory and industry responses added complexity. The Trump administration’s broader maritime measures, including controversial fees targeting Chinese-built or -owned vessels entering U.S. ports, prompted widespread industry opposition, particularly from U.S. exporters fearing retaliatory measures and escalating costs. Port authorities worldwide responded to shifting trade patterns with announcements of strategic infrastructure investments, notably in Mexico and Vietnam, to accommodate anticipated long-term traffic increases.

Looking forward through 2025 and into 2026, the outlook under current policy conditions suggests continued stagnation or modest decline in global maritime trade volumes. According to Drewry and the World Trade Organization (WTO), sustained tariffs are likely to depress container traffic between the U.S. and China significantly, potentially stabilizing at volumes nearly 40% below previous norms. Fuel demand is expected to remain subdued, reflecting reduced global trade flows, though regulatory drivers will continue promoting cleaner fuels like LNG and biofuel blends. Shipping companies, anticipating protracted volatility, are likely to maintain conservative fleet management, avoiding speculative expansions while refining operational agility.

As a reminder, shipping is itself a substantial consumer of fossil fuels, and economic downturns impact fossil fuel demand in multiple parts of the world. I assessed US domestic air transportation recently and found a much lower increase year over year for Q1 than predicted, only 1%, and of course the layoffs and closures sweeping through the US economy mean fewer people driving to work. In my discussion with the Jefferies investment bank host as part of the firm’s day of presentations and Q&A on the United States’ trade war, China’s reaction and the implications for global institutional investors, I added to the key theme of all presenters that long-term investments reaching final investment decision in the United States are deeply unlikely with the uncertainty, and that investments would likely be short-term, speculative and likely hype driven.

U.S. citizens aren’t traveling domestically as much to save their money or have their budgets diverted due to inflated costs. Employment is soft, if not yet contracting, with minor private sector growth matched by federal layoffs under DOGE, so no additional commuting demand. Industry and commerce are in some sectors stilling. Aviation emissions are down as the number of people visiting the country are down. Shipping fuel consumption is down. Trump is COVID-19, without the face masks. Trump: Inadvertent Climate Hero.

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy