War, Oil & Cleantech: Thoughts on the Ramifications of the USA’s Latest Imperial Adventure

Support CleanTechnica’s work through a Substack subscription or on Stripe.

It’s now been more than two months since US President Donald Trump ordered the execution of a Special Military Operation in Venezuela leading to the capture of Nicolás Maduro and the transfer of power to Delcy Rodríguez, and more than 10 days since that same president ordered the start of bombardments on Iran. The first went as smoothly as anyone could’ve hoped (I was extremely pessimistic, and, thankfully, wrong), but it seems that Trump’s luck ran out, as the second misadventure seems to be devolving into a “Forever War” that could well upend the global economic system as we know it.

Both of these attacks, military operations, wars, or whatever you want to call them involve oil-producing countries, one of which controls the largest reserves in the world, the other of which accounts for nearly 4% of global production and can at any moment blockade the strait that transports 25% of the world’s oil and 20% of its LNG. Because of this, and following our series on the future of oil in the Age of Cleantech, I figured it was time to check how things are going and what we may expect from the developments of this new adventure in US Imperialism.

Adventures in Imperialism, Part I: Venezuela’s successful regime continuance

Let’s not sugarcoat this: many of us may, in principle, condemn any unprovoked intervention from one country into another, but for the US, this was an astounding success: the operation was over in hours, the new government was willing to negotiate with the US within days, and there were basically zero ramifications. All deaths fell on the shoulders of Venezuelan and Cuban soldiers, with no US casualties. And the US basically got everything it wanted, including a subservient government, access to Venezuela’s vast oil reserves, and a media victory marked by the picture of Nicolas Maduro in chains.

Venezuela’s opposition leaders were left out of the new government, meaning in a way Trump did replace one Chavista leader with another Chavista, but by keeping Delcy Rodríguez (Maduro’s vice president) in power, he did guarantee a stable transition.

In all fairness, Maduro had already been making inroads towards the liberalization of markets, and it’s likely the US would’ve gotten a pretty similar deal had they asked. Such an agreement, though, would’ve been difficult to sell after the debacle that were the 2024 elections, so I guess Trump needed a show of force before proceeding to make a deal.

But I digress.

It’s all but certain that a civil conflict has been avoided in Venezuela, and that slowly but surely Delcy will liberalize oil and national markets, will end capital controls, and will allow for the investment of foreign funds in Venezuela, granting special rights to US companies willing to exploit its oil & gas reserves. It remains to be seen if elections will eventually be called, or if liberalization will be limited to the economic sphere.

Now, it seems that Trump expected Venezuela to become a hub for US investment in the short term, but Big Oil was unsurprisingly skeptical about making investments in the Orinoco Belt, which requires oil prices to be above $80 a barrel to make a profit. However, not all Venezuelan reserves are in the Orinoco Belt, and oil production has been slowly ramping up, adding nearly 100,000 barrels a day in February and surpassing the 1mbd mark. Most of this is heavy oil, ideal for the refineries in the Gulf of Mexico, meaning the US is likely already getting a good deal out of its adventure.

In normal circumstances, this would’ve pressured oil prices down, as Venezuela’s oil industry would be expected to add some 300,000 additional daily barrels of production. But, as we all know, we’re no longer anywhere near normal circumstances.

Adventures in Imperialism, Part II: Iran’s unsuccessful regime change

As I write these words, 12 days have passed since Israel and the US first bombed Iran with aims that aren’t completely clear. And even though it’s still early to know if this was a slight mistake, a gaffe, a grave error, or a massive blunder, I think we can all agree there was at best a significant miscalculation on Trump’s team regarding Iran’s reaction to these attacks.

At this point, most of our readers probably know what Hormuz is, but just in case: Iran sits just north of the Strait of Hormuz, which serves as a waterway to carry some 25% of the globe’s oil and 20% of its LNG. The threat of closing the strait has been for decades one of the main tools the Ayatollah and the Islamic Guard Corps have had at their disposal to prevent attacks on their country by any rational actor.

Alas, I feel the US government no longer qualifies as a fully rational actor.

Unsurprisingly, the bombardments on Iran and the death of Ayatollah Khamenei and many other leadership figures led to a rapid escalation and to the effective closure of the Strait after a couple of days. Whatever Trump and his team expected is not clear (perhaps an uprising, as the Iranian theocracy has been under severe strain in the near past due at least in part to economic mismanagement and political repression), but it’s clear they’re not getting it, as — again, unsurprisingly — people are seeing the bombardments on their country and as a result are rallying around the flag.

And this is where we stand. Iran has no hope of winning a military contest with a US+Israel coalition, but it can bomb countries that authorize the use of US military bases, and it can also sustain the blockade of the strait, perhaps indefinitely. And that, in due time, will bring the US and most of the world’s economy to its knees.

Towards the abyss

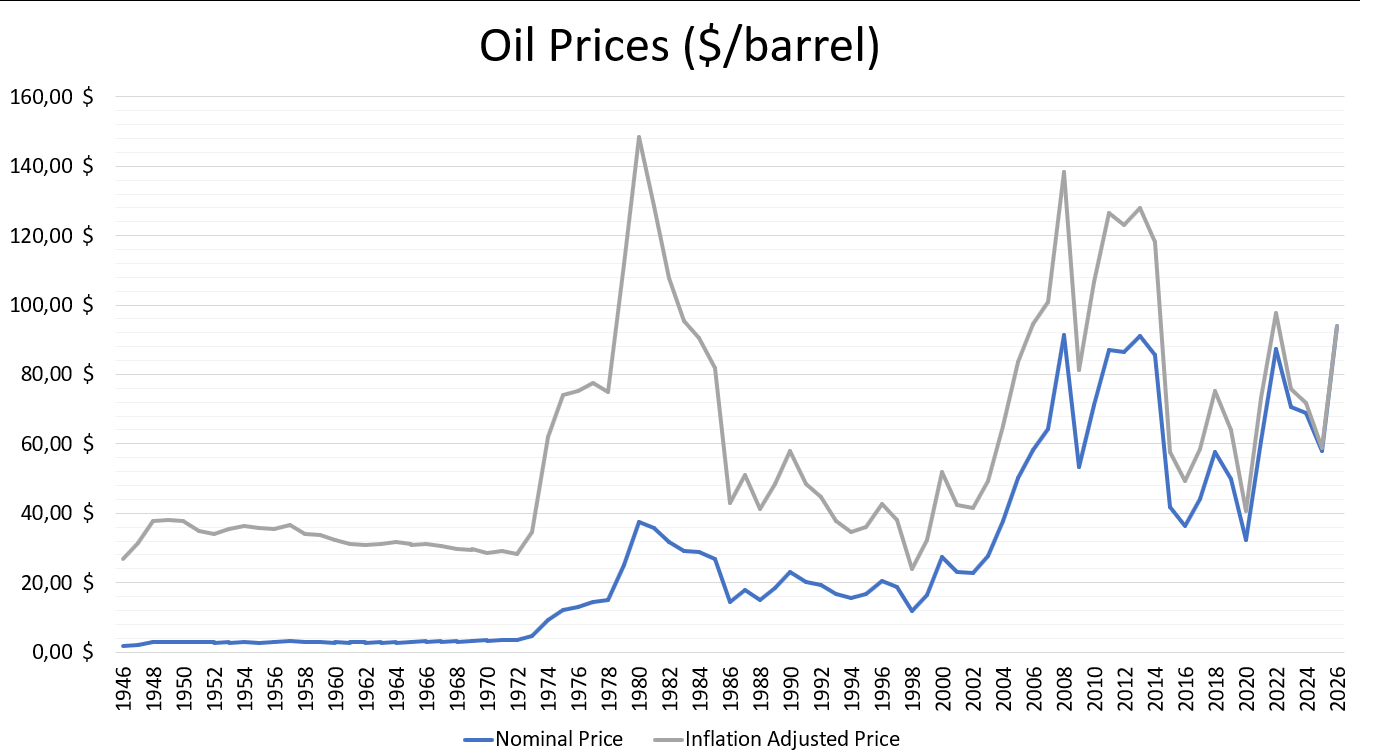

12 years ago, an excess production of around 3 million barrels a day (from a total of 90 million, this is around 3.3%) managed to bring prices from $120 per barrel to $40 in a matter of months. This reflects the lack of elasticity of oil, meaning consumption isn’t likely to rise rapidly as prices go down, and production is also not likely to rise as prices go up, thus giving relatively small swings in production or consumption a huge impact on prices.

Nowadays, the disruption is somewhere around 15 million barrels, or ~14% of global production — that is, 15 million barrels that used to be available in the market but no longer are.

Never in the history of oil have we seen such a disruption. The economic consequences of this could be profound. If this blockade holds, we could see $150, $180, or even $200 per barrel. And it’s not only oil. LNG prices have also risen sharply, as Hormuz is even more relevant to gas than it is to oil. Gas prices have roughly doubled, putting pressure on countries all over the world that depend on this commodity to keep the lights on.

No country can replace such a gargantuan amount at such short notice. At best, the US may add some 600,000 barrels of production in the next few months, and Venezuela some 300,000. Other countries may add up to 1 or perhaps 2 million extra barrels, and that amount could double by 2027 … meaning in the best of cases we would still be 9 million barrels a day short of what used to be global oil production.

Historically, high energy prices have a very high correlation with economic recessions. If the blockade holds, we can be certain economic activity will grind to a halt, eventually bringing fossil fuel consumption — and thus prices — down again. Those reductions in oil demand have always been temporary. Eventually, economic activity ramps up again and oil demand picks up, but the phenomenon of “demand destruction” due to high prices is a well documented one, and it’s the one I wish to focus on.

As this time, I believe, it’s different. For never in the history of energy have alternatives existed, capable of economically replacing so many of the uses we have for oil and gas.

A brief history of oil crisis & demand destruction

Back in the 1970s, the oil shocks of 1973 and 1979 created the perfect storm for a “lost decade” for oil demand, which in 1985 was still below what it had been in 1973. Likewise, the high prices of oil in the 2000s were very likely related to the 2008 financial crisis and economic downturn, meaning the second half of the decade was pretty much lost for oil demand growth. Global oil demand grew by 10% between 1995 and 2000 and by 8% between that year and 2005, but only by 1% between 2005 and 2010.

Proper “demand destruction” mainly happened in the years of economic crisis, this is: 1973-74, 1979-83, and 2008-2009. But even without economic downturns, we find oil demand stagnating in the years with high oil prices, particularly 2004-2008, as economic actors tried to insulate themselves from them and provide economic value with less fossil fuel inputs.

This visibly happened in 2004 and not in 1973 because the economy was far less oil-intensive in 2004 compared to 1974 (as Paul Krugman argues)… and even less so in 2026 than in 2006.

To give an example regarding passenger transport: a country in 1975 could only insulate itself from high fuel prices with expensive electrified public transport infrastructure (read, trains, trams and trolleys) and then either building nuclear plants or somehow hydroelectric dams to run those. In 2026, there are e-bikes, EVs and E-Buses at prices comparable to their fuel counterparts, which can be recharged by solar and wind energy that’s cheaper than gas or coal (and much cheaper than fuel). And every e-bike. EV and E-Bus purchased translate into oil that will never be purchased and burnt.

Based upon this, I think we can conclude demand destruction will last this time around. But how much destruction will there be? Well, nobody has a crystal ball, but to guess how oil demand will behave, we can look into history for a guide.

In 1973, adjusting for inflation, oil rose to $35 a barrel, and kept going up all the way to $75 a barrel in 1976. It wasn’t too much compared to current levels, but it was at a time when the economy was extremely oil-intensive, and consumption fell slightly (3%) by 1975 before recovering in 1976.

In 1979, the shock was much worse. Oil prices surpassed $110 (eventually reaching almost $150 in 1980) and would sustain those levels for the next four years. As a result, demand cratered, falling 6% between 1979 and 1985, and only fully recovering by 1988.

Prices would not reach $100 per barrel again until 2007. Demand destruction in this period happened only through the 2008 financial crisis, thanks to strong public investment to recover from the global financial crisis and thanks to China’s resilience. After this, Chine would become the leading market driving oil demand growth.

At last, we found prices very close to $100 again in 2022, but by then the world was recovering from the Covid-19 pandemic, which meant oil demand was simply recovering previously lost growth.

From this, we can conclude a couple of things. First, the world seems to have gotten more resilient and more capable of sustaining high oil demand even amidst high prices, though a large part of this (after the 2008 financial crisis and after the 2022 oil shock) was financed with debt.

And second, it seems that a few months of high oil prices will not be enough to create sustained demand destruction, which reached its highest after 1979 and involved seven continuous years of the highest oil prices recorded since WWII.

So, with this in mind, what’s coming next?

The future of cleantech & oil (and gas)

Most of our forecast depends on how long the war lasts, and, crucially, how long the strait remains closed. Nobody can know that for certain, and even if it’s clear that the war has lasted far longer than expected by Trump and his team, it may be that the Islamic Republic of Iran reaches a negotiated settlement next week, or that hostilities don’t end and it keeps Hormuz closed for a few years.

What we do know is that the scale of the disruption is something yet unseen. The release of 400 million thousand barrels from IEA reserves is an indication that the countries comprising this institution don’t seem to believe the war will be short.

The immediate impact, first and foremost, will be sociopolitical. There have been many oil crises in history, but this is the first one where an alternative source of mobility at or near price parity with the traditional fuel-based one is available for governments and millions of consumers. Already we see interest picking up in the countries where gasoline prices have risen, and this crisis, should it last more than a few weeks, could have lasting impacts in the vehicle markets of most of Europe, of Australia, of Chile, to name a few. It’s possible some oil-importing countries will go the way of Ethiopia to prevent further disruptions from these incidents.

But as war goes on (assuming it does), and as oil prices rise, a sense of urgency will grow: countries during the 1979 and even the 2008 oil shocks did not have alternatives, but we do. And since the scale of the disruption is at a level prior unseen, it’s likely things will get very dramatic, very fast. How long before many countries start taxing ICEV imports to prevent further damage from currency-account deficits? How long before a few outright ban them?

A lot will depend on how high prices get. $110? There will be disruption for sure, but perhaps the world will avoid a recession and some communities may choose to buckle up and ride the wave rather than change their way of living. $150? Yeah, things will get tougher, and if that goes on longer than a few weeks, it will almost certainly bring the global economy to a halt. $200+? That’s uncharted territory. At those prices, demand destruction will likely be decisive, the economic crisis will be severe, and air and sea transport will suffer.

I have mostly touched on oil, but most of the things said before also apply to gas, only this time it’s not EVs, but wind turbines and — crucially — solar panels that may serve as a realistic alternative. Like oil, gas is critical for most nations, and those who lack either local wells or access to gas pipes will likely feel the pinch.

Final thoughts

OPEC just published its March Monthly Oil Market Report, and, unsurprisingly, it keeps the expectation for oil demand growth in 2026 at +1.34 million barrels a day, the same forecast as in February. It seems they refuse to believe that an oil shock may cause any changes whatsoever to oil demand. Or perhaps they expect the war to end in the next couple of days, which to be fair is a possibility (though, I’d argue even then we would see some impact, as at least some actors will try to protect themselves from future disruptions).

Instead, I believe we will see the disruption from cleantech accelerate as oil and gas prices remain through the roof. China’s so called “overcapacity” in solar panel and EV production will no doubt come in handy here as the country profits from the world’s need to reduce oil dependence.

As always, I like to present at least a rough forecast to try and see if I hit the bullseye. In this case, if the IEA was calculating global oil demand growth for 2026 at some 850,000 barrels a day, I’d think that number could very well halve if oil remains above $110, and it could become negative above $125 through the rest of the year.

The countries that are leading oil demand growth right now — India and China — are likely to pivot. China now has all the infrastructure in place to rapidly reduce oil consumption, whereas India is just starting this process, but it’s also likely to suffer a much larger shock due to high oil and gas prices, and therefore will probably act decisively to minimize damage. This will also apply for a lot of developing economies in Asia, which is the third region leading oil demand growth according to OPEC.

As for gas, well, it’s a tougher nut to crack. Countries with available gas wells and/or access to gas pipelines will remain insulated from the chaos and may even profit as their energy prices remain low and their industries become more competitive. But large importers of LNG will likely go the way of Pakistan as fast as they materially can.

All in all, as so many other CleanTechnica writers have mentioned, this is a crude reminder why energy independence is important, and why relying on global commodities that depend on a 33-km wide strait is insanity.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy