Why ShippingŌĆÖs Low-Carbon Future Relies More on Batteries & Biofuels Than Methanol

Maritime shipping, responsible for approximately 3% of global greenhouse gas emissions, stands at an unprecedented turning point. As we progress toward mid-century, decarbonization is no longer optional but mandatory, driven by stringent international regulations, including the International Maritimate OrganizationŌĆÖs recent fuel carbon pricing decision and corporate sustainability commitments. This requirement for transformation in shippingŌĆÖs propulsion systems has elevated a handful of fuel and technology pathways into contention: methanol, biodiesel and hydrotreated vegetable oil (HVO), and battery-electric propulsion. Each of these options presents unique economic, logistical, and operational tradeoffs that shape their viability in the decades ahead.

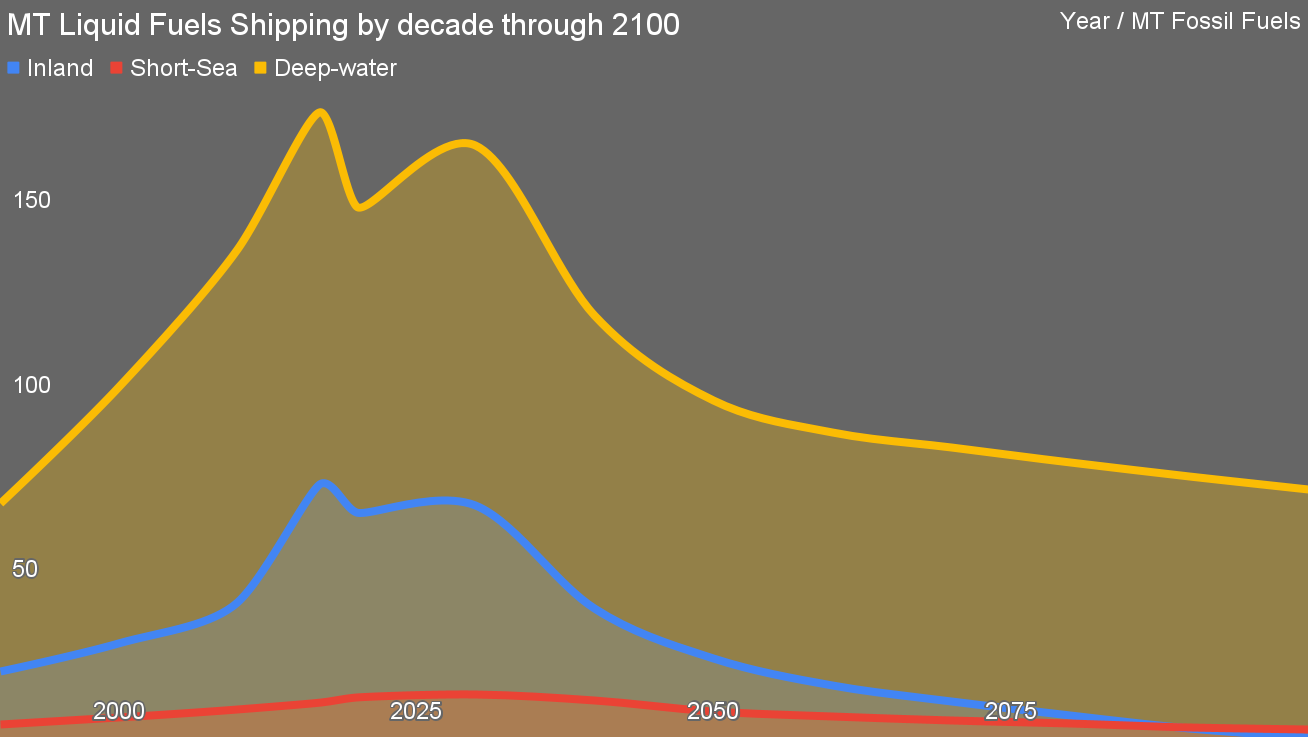

Analyzing shipping decarbonization through 2100, my projections see an aggressive shift away from traditional fossil fuels. These scenarios anticipate near-complete displacement of heavy fuel oils by biomoass-derived alternatives and electrification. The broader decarbonization trajectory indicates a gradual but definitive movement toward low-carbon and zero-emission shipping, driven primarily by intensifying regulatory frameworks, carbon pricing, and market expectations.

Methanol-fueled ships have recently captured significant attention within the maritime industry. 60 dual-fuel methanol ships are currently in operation and approximately 340 dual-fuel vessels are on order globally as of mid-2025, reflecting rapid and aggressive adoption among major shipping companies, particularly container ship operators such as Maersk, CMA CGM, COSCO, ONE, and Evergreen. These dual-fuel vessels represent a strategic hedge by shipowners and operators against future carbon pricing risks and stricter emissions regulations. However, the high enthusiasm seen in vessel orders contrasts sharply with the sobering reality of methanol fuel supply.

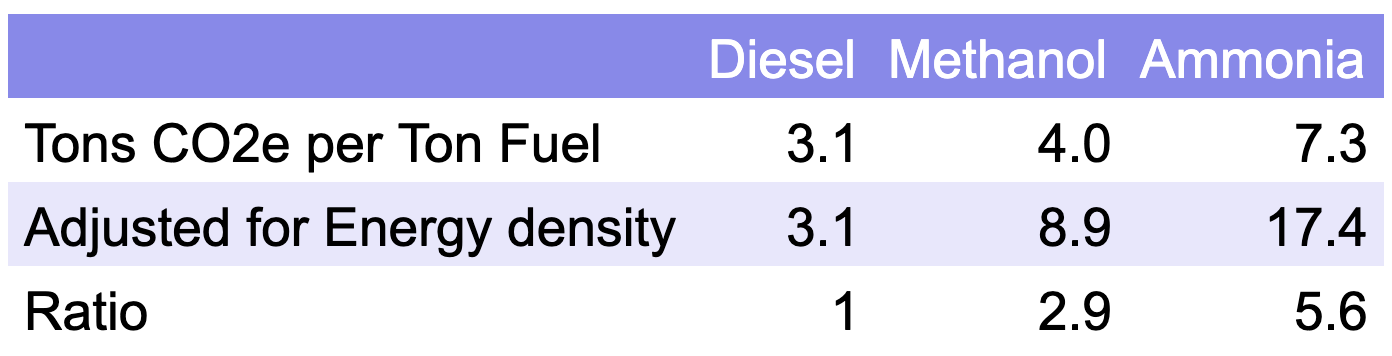

Low-carbon methanolŌĆöeither biomethanol produced from renewable biomass or e-methanol synthesized from captured carbon dioxide and renewable hydrogenŌĆöis today scarcely available and extremely costly. Current global renewable methanol production is negligible, less than 1% of total methanol production, and substantially insufficient to support the burgeoning methanol-fleet. With biomethanol prices typically between $1,200 and $1,500 per ton, and e-methanol even higher, around $1,500 to $2,000 per ton, the economic challenge of large-scale adoption is pronounced. ItŌĆÖs important to note that methanol has only 45% of the energy density of VLSFO, so the prices per kilometer steamed are much higher than a per ton cost assessment would suggest. As a result, methanol-capable ships, despite their potential, presently consume predominantly fossil-based methanol or conventional marine fuels.

As I worked out a couple of years ago, fossil-derived methanol isnŌĆÖt remotely a climate solution, although it is a pollution solution. As 99.5% of methanol is derived from natural gas or coal gas, the average carbon intensity is almost three times that of VLSFO or marine diesel. Natural gas derived methanol is only double the emissions, but that still has zero merit. The methanol industry has long been using much better tank-to-wake numbers instead of appropriate well-to-wake numbers to pretend itŌĆÖs a clean fuel. The IMO only adopted well-to-wake requirements for decarbonization assessments in 2021, something the methanol and ammonia industries exploited, along with the global delusion that green hydrogen would be cheap, to pretend that they were the right choices.

Logistical constraints compound the challenge for low-carbon methanol adoption. Shipowners have reported difficulties securing consistent, reliable sources of renewable methanol, reflecting a broader infrastructural bottleneck. Ports capable of supplying renewable methanol remain few, with operators encountering complex logistical and safety considerations that complicate rapid deployment. Early adopters, notably Maersk, have had to invest considerable effort and resources into arranging limited, high-cost supplies of renewable methanol for initial voyages, highlighting the nascent state of bunkering infrastructure and the prohibitive costs associated with these pioneering endeavors.

By comparison, biodiesel and hydrotreated vegetable oil (HVO) are notably pragmatic and immediately deployable alternatives. Both fuels, produced from waste biomass and vegetable oils, leverage established refining processes, mature supply chains, and existing marine fuel infrastructure. Their ŌĆ£drop-inŌĆØ nature is crucialŌĆömarine diesel engines can use biodiesel and HVO blends without modifications, significantly reducing barriers to adoption. Furthermore, biodiesel and HVO prices are considerably lower and more predictable than those for low-carbon methanol, typically around $1,000 to $1,500 per ton.

Importantly, the ongoing electrification of road transport is projected to free substantial volumes of biofuels initially allocated to ground vehicles, enhancing future maritime availability and possibly driving costs even lower over time. As the IEA reported last year, we already manufacture about 100 million tons of biofuels, 70 million tons of it HVO and biodiesel, every year, but we use it almost entirely in ground transportation today. IŌĆÖve had the conversation with the leaders of the US biodiesel association, and they are looking closely at maritime shipping as their next growth market.

That drop in nature includes bunkering facilities in ports. Blends of VLSFO and biodiesel/HVO are available in some parts today, with exactly the same short side tanks and bunkering processes delivering the blends instead of pure VLSFO. By contrast, methanol requires new tanks, new processes, and new pumping equipment, or extensive modifications to existing equipment due to its much more corrosive nature. Lower capital and operating costs for ports and ships make HVO/biodiesel an easy choice compared to methanol of any provenance.

ThereŌĆÖs an argument to be made here that while ships can run on methanol, airplanes canŌĆÖt, and that the heavier molecules in feedstocks easily transformed into HVO, biodiesel or biokerosene must be preserved for aviation. Paul Martin and I have had that discussion a few times. However, as there are so many pathways to biofuels of all types, including human poop to jet fuel, IŌĆÖm content to let this one play out in the marketplace. One of my business collaborators is approaching final investment decision on a methanol-to-jet plant on refinery grounds in the UK, with sourced biomethanol as the feedstock, and LanzaJet is constructing a million gallon a year ethanol-to-jet plant in the United States. The jury is out.

Battery-electric propulsion presents a compelling long-term solution, particularly for shorter-distance shipping routes, ferries, coastal vessels, and inland waterway transport. Battery prices have declined dramatically over the past decade, and continued steep reductions are projected. While battery propulsion systems still entail significant upfront capital investment, primarily due to battery pack costs, these expenses amortize effectively over the multi-decade lifespan typical of maritime vessels. Battery-electric propulsion boasts unmatched energy efficiencyŌĆöaround 80ŌĆō90%, vastly superior to internal combustion engines. Beyond economic considerations, battery-electric ships have near-silent operation, minimal maintenance needs, and elimination of direct emissions, making them particularly suited for environmentally sensitive areas and ports.

For larger, ocean-going ships with extended range requirements, full battery-electric propulsion remains impractical in the short to medium term due to battery size, weight, and cost constraints. However, hybrid propulsion systems that integrate batteries with biodiesel or HVO engines represent a powerful interim solution. In such hybrid configurations, onboard batteries cover peak energy demands, manage variable loads efficiently, and provide significant operational savings through optimized engine efficiency. Such hybrid systems extend battery advantagesŌĆöhigh efficiency, reduced emissions, and noise reductionŌĆöto longer-distance vessels, facilitating regulatory compliance and reducing overall lifecycle operating costs.

Regulatory environments increasingly define maritime operational contexts, notably through the expansion of Emissions Control Areas (ECAs). These areas, prevalent in Northern Europe, North America, and now growing rapidly in Asia, impose strict standards on fuel sulfur content and emissions, fundamentally reshaping fuel and technology selection. Crucially, methanol (particularly renewable), biodiesel, HVO, and battery-electric propulsion all comply fully with ECA regulations, providing fleet operators substantial flexibility and reduced regulatory risks.

My current expectation is that all ships will have battery electric drive trains, with ocean-crossing vessels hybridized. All shipping will operate on batteries within 200 km of coasts, in ports and on in land water ways in the end game. Whether the hybrid fuel is HVO/biodiesel or bio-methane remains to be seen.

A comprehensive comparison of fuels must factor in both energy densities and engine efficiencies. Adjusting for these critical elements clearly reveals battery electric as the lowest operating cost alternative to VLSFO with biodiesel and HVO as the most economically practical solutions among the renewable liquid fuels. This calculation today was readily available to be done years ago when I first did it, and the shipping industry isnŌĆÖt a charity. Decarbonized ships will operate on what is cheap, available and low-carbon, and thatŌĆÖs not methanol.

That e-methanol price point isnŌĆÖt going to get better. As IŌĆÖve been pointing out for years, hydrogen can be green, but it canŌĆÖt be cheap, most recently in a piece outlining five energy myths. Synthetic fuels will remain much more expensive than biofuels. Further, the price gap between biomethanol and biodiesel/HVO isnŌĆÖt going to close much, if at all.

As a note for ammonia advocates, I remain astounded that anyone is considering the liquid as a shipping fuel. Mariners can tell what engines are burning because of the smell in the engine room due to slippage. Ammonia fumes are incredibly dangerous to humans, often lethal. When ammonia mixes with water ŌĆö note, these are ships we are talking about ŌĆö ammonia turns into a highly corrosive gas which if inhaled destroys lungs. After that it turns into something thatŌĆÖs just bad for human health. As one European public health official pointed out, if there were a major bunkering spill, tens of thousands of people in port cities would die. Then thereŌĆÖs the danger to marine life. Yes, we have ammonia tankers, but only a few dozen, and they are dealt with in separate areas of ports with extreme care.

Ammonia is a great fertilizer, and using it that way maximizes crop yields which can then be used for biofuels. Using a ton of ammonia to grow crops rather than burning it yields roughly forty-times more usable fuel energy (and around thirty times the mass of liquid fuel). Low-carbon ammonia will be expensive ammonia and it canŌĆÖt be made from biomass, so it will be in the same price range as e-methanol, far out of the running.

Evaluating these options and market dynamics, the pragmatic reality is increasingly evident. Methanol-capable dual-fuel ships offer essential flexibility but, given renewable methanolŌĆÖs limited availability, challenging logistics, and high costs, these ships are likely to rely predominantly on fossil methanol or conventional fuels in the short term, limiting their environmental benefit. IŌĆÖve said for years that these dual-fuel ships will likely burn a lot more HVO/biodiesel than methanol in their lifetime, and I see little reason to change my opinion so far.

Conversely, biodiesel/HVO hybridized with battery-electric propulsion represents the most cost-effective, operationally viable, and immediately impactful route to substantial decarbonization. These hybrid systems reduce emissions, optimize energy efficiency, and significantly lower operational costs, positioning them as the preferred transitional and possibly permanent solution for substantial segments of the maritime industry.

ShippingŌĆÖs decarbonization trajectory through 2100 will be defined not by any single fuel or technology, but by a flexible and pragmatic mix of biodiesel, HVO and batteries. Operators and investors who embrace pragmatic hybrid solutions today stand not only to reduce environmental impacts significantly but also to position themselves advantageously for a future where regulatory certainty, economic viability, and environmental sustainability align decisively.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy